A credit card debt consolidation loan becomes a necessity when you fail to pay off your credit card dues on time. In this situation, you pay a high interest rate on your unpaid dues. If you can get a loan at a reduced interest rate, you can easily pay off your dues and save some money on interest. However, you need to have a good credit score in order to become eligible for a low interest rate. If you check your credit score, you will know whether it can get you a low-interest loan.

What is Debt Consolidation?

Consolidating multiple debts into a single loan is called debt consolidation. You can take it as a real help from a friendly financier. The financier agrees to lend a loan at a reduced interest rate to help you pay off your dues. However, this loan isn’t free from conditions. The first condition is having a good credit score. Your credit profile says many things about your financial health. A good profile strengthens reliability and attracts financiers. A poor credit score can also get you a loan, but at a slightly higher interest rate.

Understanding the Importance of a CIBIL Score

It is a three-digit number that reflects your credit profile. You can also call it a fact check of your creditworthiness. In India, it is checked on a scale of 300 to 900. Every lender checks the credit profile of potential borrowers when processing loan applications.

Check your credit profile:

- 750 and above: Excellent

- 700-749: Good

- 650-699: Fair

- Below 650: Average

An excellent credit score makes you eligible for the lowest debt consolidation interest rates, but an average score puts you in the high-risk category for lenders. They will increase the interest rate to cover their risk.

Can You Still Get a Debt Consolidation Loan?

While a credit score is an important factor in debt consolidation, an average score can’t impact your overall credibility. You can still get a low-interest loan to consolidate your debt. Lenders assess the credibility of potential borrowers on certain factors, including credit score. However, they form an opinion on borrowers with average credit scores only after checking other factors.

1. Stable Income

Stability of income is a bigger factor than credit score. It shows that you can improve your credit profile by paying off your dues. You get a fixed income every month. Lenders take your fixed income as a guarantee that you will never default on your loan payments.

2. Employment History

If you have been working with your present company for a long time or have a stable business, your profile is of interest to lenders. They will give loans even if your credit profile is average. A credible employment history can cover the gap created by your credit score.

3. Debt-to-Income Ratio

If your monthly income is already committed to debt payments, your debt-to-income ratio is low. But if you can save some cash after paying your debt payments, your debt-to-income ratio is high. It can make you eligible for low interest rates.

4. Existing Relationship with Lenders

Have you ever borrowed a loan from a bank or private financier? If yes, then you can leverage your relationship for debt consolidation. If you paid the loan on time, the lender may consider it as a strong debt consolidation loan eligibility.

How to Improve Your Chances of Approval

You need to take precautions when applying for debt consolidation. With an average credit score, it won’t be a cake walk for you.

1. Check Your Credit Report

Check your credit score from a reliable and authorized agency and download a detailed report. The report will show your credit profile with all active loans. It will give you a detailed idea of your eligibility for a multiple EMI to single EMI loan.

2. Reduce Outstanding Credit Card Balances

High credit card utilization shows your over-dependence on credit money. It makes you highly unreliable for lenders. However, paying down existing balances will show your commitment to paying off all your debts.

3. Avoid Multiple Loan Applications

Submitting loan applications to multiple lenders, especially with an average credit score and high credit card utilization can go against your favor. It will hit your creditworthiness and make you unreliable for lenders. Submit one balance transfer loan application at a time and wait for the lender to respond before approaching others.

4. Consider a Co-Applicant

Adding a co-applicant with a good credit score to your loan application can enhance your creditworthiness. Lenders will rely on the co-applicant and approve your application. It is how many people get low-interest loans when they are in need.

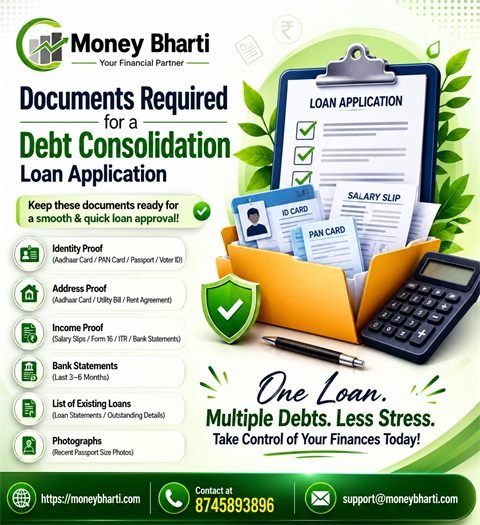

5. Provide Complete Documents

Attach all the necessary documents to your loan application. Also, be ready to furnish papers as required by the lender. The financier will process your application on the basis of your papers. If you provide complete documents, the lender will be able to determine your creditworthiness.

Should I take a Loan with Average Credit Score

A balance transfer loan with an interest rate much lower than a credit card’s interest rate is a better idea. An average credit score may not get the lowest interest rate, but it will certainly lower your interest rate in comparison to credit cards. You will have all the benefits of debt consolidation. You will pay a single EMI instead of multiple, save on interest, and be debt-free.

Final Thoughts

An average credit score reduces your options, but it certainly doesn’t bar you from consolidating your debt. Also, you can improve your credit profile by limiting your card utilization and increasing your payments. Meanwhile, you can try other options to consolidate your debt into a single, low-interest loan.

Use a debt consolidation EMI calculator to calculate your savings after consolidating your debts. If you find it lucrative, you can go ahead to consolidate your debts. Here, a loan agency can help. The advantage of hiring a loan agent for loan consolidation is that you have access to a wide range of financiers.