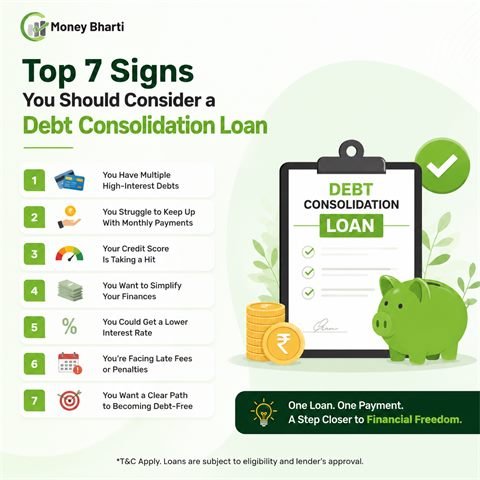

Consolidating debt is a trustworthy way to manage debt. It simplifies debts from multiple EMIs to a single EMI loan. For this reason, it is better suited for multiple debts, especially credit card dues. If you have incurred a huge debt and pay multiple times every month, consider consolidating your debts into a single, low-interest loan. This blog will help you understand the basics of debt consolidation, its benefits, and eligibility.

What is Debt Consolidation?

It is a loan, but with the lowest interest rate. Its objective is to club all your EMIs into a single loan. A lower interest rate not only reduces the monthly payment but also the total payment. It saves money in the long. It can help you become debt-free within a fixed time. The good thing is that you can get a new loan even if your credit score is low. An experienced loan agency can help get a quick loan.

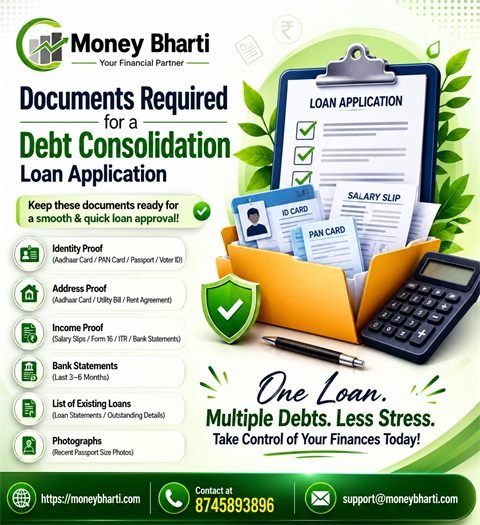

Before you start your journey to become debt-free, understand debt consolidation loan eligibility. Lenders have varying requirements for borrowers. However, the conditions vary from one lender to another; there are some common requirements you need to fulfil at the time of lodging your loan application. This blog will serve as a detailed guide for loan consolidation.

Basic Eligibility Criteria

While requirements vary among lenders, some requirements are common. Check whether you meet these conditions. Also, learn ways to increase your eligibility for loan consolidation. If you’ve any queries, you can approach an experienced loan agency for help. Loan agents work closely with lenders. They can help find loans you qualify for.

1. Age Requirement

Banks, Non-Banking Finance Companies, and private financiers have agreed to set the age limit for new loans from 21 to 60 years. However, the upper age limit can be relaxed in specific conditions, such as employment status, retirement plans, and present assets. If you are already 60 or near the upper age limit, you can discuss a credit card debt consolidation loan with your loan advisor. The advisor may find a suitable loan for your needs.

2. Employment Status

Your employment status is of interest to lenders. It provides a better idea of your monthly income and financial stability. Lenders want to know the nature of the work you do.

- Government employee

- Employed with a private company

- Self-employed (Freelancer)

- Businessman

If you’re a government employee, you won’t have to submit many papers to prove your employment. However, self-employed individuals and businessmen need to prove their employment from their tax receipts.

3. Monthly Income

Stable employment demonstrates regular income and repayment capacity. It reduces lending risk. For this reason, debt consolidation for salaried employees is much easier than for others. But never mind, if you’re self-employed or a businessman. If you meet the following requirements, you can get a loan.

- Regular monthly salary

- Consistent business income

- Profitable freelancing

- Adequate disposable income after existing liabilities

A higher income—whether from salary or business—shows lenders you can repay borrowed money, improving your eligibility for quick loans at the lowest interest rate.

4. Credit Score

You need a healthy credit score to be eligible for a loan, especially for low-interest borrowing. Your credit score decides your interest rate. You can check your credit score for free; however, it is more important to learn how to improve your credit score.

Understanding Credit Score:

- 750 and above: Excellent

- 700-749: Good

- 650-699: Moderate

- Below 650: Average

An excellent credit score can get you the lowest interest rate. Conversely, loan consolidation with an average score may cost you dearly in terms of interest rates.

5. Debt-to-Income Ratio

It is an important factor showing the difference between your monthly earnings and debt payments. If it is low, you have a higher chance of getting quick approval. If your DTI is high, you need to work on it.

Example:

Your monthly income is ₹1,00,000, and your total debt payment is ₹30,000. Your DTI will be:

- 30000/100000 x 100 = 30%

With 30 DTI, you’re a valuable client for lenders. But if it drops to 20% or lower, the lenders may disapprove your loan or increase debt consolidation interest rates.