1. Introduction

Credit card debt builds up quietly. A few purchases here, an emergency expense there, and before long the minimum payments across three or four cards start eating into a paycheck without making much of a dent in what's actually owed. That's the nature of revolving credit: high APRs mean a large share of every payment goes toward interest rather than principal, so balances can feel stuck in place for years.

This is exactly why so many people look into a debt consolidation loan or another consolidation route instead of continuing to juggle multiple cards. Combining several balances into a single payment, ideally at a lower interest rate, can simplify a budget, reduce financial hardship, and shorten the runway to becoming debt-free. It isn't the right move for everyone, and it isn't free of trade-offs, but for many households carrying high-interest, multi-card debt, it's one of the more practical debt relief strategies available.

This guide walks through what credit card consolidation actually is, how it works, the main types of programs, who tends to benefit most, what it costs, and how it compares to alternatives like debt settlement. It also covers eligibility, a step-by-step application process, common mistakes to avoid, and a short decision guide to help narrow down the right option for your situation.

2. What Is a Credit Card Consolidation Program?

Simple Definition

A credit card debt consolidation loan or program is any financial strategy that combines multiple credit card balances into a single debt obligation, usually with one monthly payment, a fixed loan term, and often a lower interest rate than the original cards.

How It Works

Instead of making separate minimum payments to several different card issuers each with their own due date and APR, a consolidation loan or program pays off those balances directly (or the individual continues carrying the cards but stops using them) and replaces them with one structured repayment plan.

Real-Life Example

Consider someone carrying balances on three credit cards: $4,000 at 24% APR, $2,500 at 22% APR, and $1,500 at 19% APR — a total of $8,000. Instead of making three minimum payments a month, they take out a fixed-rate personal loan for $8,000 at 12% APR over four years. The old cards are paid off in full, and the borrower now makes one predictable monthly payment at a meaningfully lower average interest rate.

3. How Credit Card Consolidation Works

Most consolidation programs follow the same basic mechanics, regardless of which option is used:

- Existing debts combine: Multiple card balances are rolled into a single new loan, credit line, or repayment plan.

- Single monthly payment: Instead of tracking several due dates and minimums, a multiple EMI to single EMI loan means there's one payment to one lender or agency.

- Lower interest rate: Because credit cards charge some of the highest consumer interest rates, most consolidation tools are designed to lower the effective APR.

- Fixed repayment schedule: Personal loans and debt management plans typically come with a defined loan term (for example, 2-5 years), giving a clear payoff date instead of open-ended revolving debt.

4. Types of Credit Card Consolidation Programs

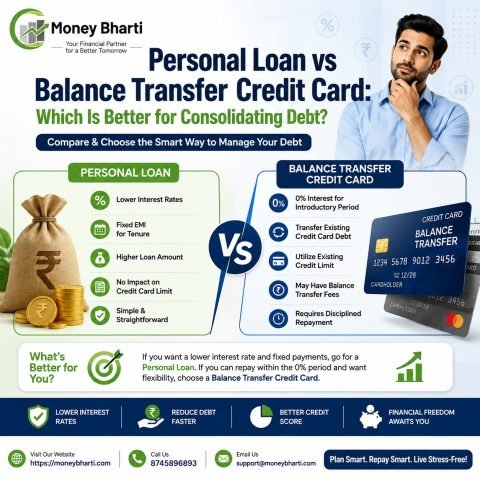

Balance Transfer Credit Cards

A balance transfer loan or card offers a promotional 0% or low APR for a set period (commonly 12-21 months) on balances transferred from other cards. A balance transfer fee (typically 3-5% of the amount moved) usually applies. This works best for people who can realistically pay off the balance before the promotional period ends, since the rate jumps significantly afterward.

Personal Loans (Unsecured Personal Loan)

An unsecured personal loan for debt consolidation from a bank, credit union, or online lender pays off card balances and replaces them with fixed monthly payments at a fixed APR over a set loan term. No collateral is required, and approval depends mainly on credit score, income, and debt-to-income ratio.

Debt Management Plans (DMP)

Offered through nonprofit credit counseling agencies, a DMP negotiates reduced interest rates and sometimes waived fees with card issuers directly. The borrower makes one monthly payment to the agency, which distributes it to creditors. DMPs usually run 3-5 years and typically require closing the enrolled credit cards.

Home Equity Loans or HELOCs (Where Relevant)

Homeowners with sufficient equity can use a home equity loan or home equity line of credit to pay off card debt, often at a lower rate than unsecured options. The trade-off is that the home becomes collateral, so missed payments carry a much bigger risk than with unsecured debt.

Debt Settlement (Not the Same as Consolidation)

Debt settlement is fundamentally different from consolidation. Rather than paying off the full balance at a lower rate, a settlement company (or the individual) negotiates with creditors to accept less than what's owed — often after the accounts have gone delinquent. This can significantly damage credit scores and may have tax implications, since forgiven debt can be considered taxable income. It's a higher-risk path typically considered only when consolidation isn't realistic.

5. Benefits of Credit Card Consolidation

- Lower interest rates: Moving from card APRs (often 20%+) to a personal loan or promotional rate can cut interest costs substantially.

- One monthly payment: Simplifies budgeting and reduces the chance of missing a due date.

- Better budgeting: A fixed monthly payment and fixed loan term make it easier to plan finances and track progress.

- Faster debt payoff: Because more of each payment goes to principal instead of interest, the debt payoff strategy tends to be faster than minimum-payment cycles.

- Credit score improvement (possible): Reducing the credit utilization ratio on revolving accounts and making consistent on-time payments can help credit scores recover over time.

6. Drawbacks of Credit Card Consolidation

- Fees: Balance transfer fees, loan origination fees, or DMP setup/monthly fees can add to the overall cost.

- Longer repayment period: A lower monthly payment sometimes comes from stretching the term out, which can mean paying more in total interest over time.

- Missed payments impact: Defaulting on a consolidation loan or DMP can undo the benefit entirely and further damage credit.

- Eligibility requirements: The best rates go to borrowers with good credit; those with poor credit may not qualify for the most favorable terms.

7. Who Should Consider Credit Card Consolidation?

Consolidation tends to make the most sense for people who have:

- High-interest debt spread across revolving credit cards

- Multiple credit cards with separate due dates and minimums

- Stable income that supports a new fixed monthly payment — this is one reason debt consolidation for salaried employees tends to be more straightforward to qualify for

- A good credit score, which unlocks better loan or balance transfer terms

Those already struggling to meet minimum payments, or without a documented income to qualify for new credit, may be better served by a nonprofit debt management plan or credit counseling before pursuing a loan-based option.

8. Eligibility Requirements

Before applying, it's worth reviewing the typical debt consolidation loan eligibility criteria lenders look at:

- Credit score: Most unsecured personal loans and balance transfer cards with the best APRs require good to excellent credit (roughly 670+), though some lenders work with fair credit at higher rates.

- Income: Lenders want to see steady, verifiable income sufficient to support the new payment.

- Debt-to-income ratio: A lower ratio of monthly debt payments to gross income improves approval odds and rate offers.

- Existing debts: Lenders review current balances, credit utilization, and payment history across existing accounts.

9. Best Credit Card Consolidation Options (U.S.)

Personal Loans

Banks, credit unions, and online lenders all offer unsecured personal loans specifically marketed for debt consolidation, often with fixed rates and terms from 2-7 years. Some lenders even offer an instant debt consolidation loan with quick approval for eligible borrowers.

Balance Transfer Cards

Major card issuers offer 0% intro APR balance transfer cards, which can be a strong option for borrowers confident they can repay the balance within the promotional window.

Non-Profit Credit Counseling

Agencies accredited by the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA) offer free or low-cost credit counseling and can set up debt management plans.

Banks and Online Lenders

Community banks, credit unions, and fintech lenders each have different underwriting standards, so comparing APR, fees, and loan terms across a few online debt consolidation services is usually worth the extra time before applying.

10. Credit Card Consolidation vs. Debt Settlement

| Feature | Consolidation | Debt Settlement |

| Credit Score Impact | Minor, short-term | Major, long-lasting |

| Interest | Lower, fixed rate | Not applicable — balance is negotiated down |

| Monthly Payment | Fixed | Negotiated, often irregular |

| Risk Level | Low | High |

Suggested Image: Debt Comparison

11. Steps to Apply for Credit Card Consolidation

- Calculate your total debt across all cards, including balances and APRs.

- Check your credit score to understand which options you're likely to qualify for.

- Compare lenders — look at APR, fees, loan term, and use a debt consolidation EMI calculator to estimate total cost.

- Apply for the loan, balance transfer card, or DMP that best fits your numbers.

- Pay off the old cards using the new loan or transfer, confirming each balance hits zero.

- Make monthly payments consistently on the new, consolidated debt until it's paid off.

12. Common Mistakes to Avoid

- Using the old cards again: Running up new balances on cards that were just paid off defeats the purpose and can leave someone worse off than before.

- Ignoring fees: Origination fees, balance transfer fees, and DMP fees all affect the real cost — not just the advertised APR.

- Only looking at the monthly payment: A lower payment stretched over a longer term can mean paying more in total interest.

- Not reading the terms: Promotional rates expire, some loans have prepayment penalties, and DMPs may require closing accounts — all details worth reading closely before signing.

13. Frequently Asked Questions

Does consolidation hurt your credit?

There's usually a small, short-term dip from the credit inquiry and new account, but consistent on-time payments and lower credit utilization tend to help scores recover — and often improve — within a few months.

Is debt consolidation worth it?

Generally, yes, if you qualify for a lower rate than your current cards, can commit to fixed payments, and avoid rebuilding new card debt afterward.

How long does it take?

Personal loan or balance transfer approval can range from same-day to about two weeks. A debt management plan through a credit counseling agency typically runs 3-5 years to full payoff.

Can I consolidate with bad credit?

Yes, though the best rates are harder to access. Nonprofit debt management plans and some secured loan options remain available even with a lower credit score.

What's the difference between consolidation and refinancing?

Consolidation combines several debts into one; refinancing replaces a single existing loan with a new one, usually for a better rate or term. A consolidation loan is, in effect, refinancing applied across multiple debts at once.

14. Conclusion

Credit card consolidation isn't a one-size-fits-all fix, but for people carrying high-interest, multi-card debt with steady income, it's often a practical way to lower interest costs, simplify monthly budgeting, and set a clear payoff date. The trade-off is added fees, eligibility requirements, and the discipline required to avoid running the old cards back up.

Quick Decision Guide:

- If your primary goal is reducing interest, a debt consolidation loan may be the best choice.

- If you're struggling to make minimum payments, a nonprofit debt management plan may be more appropriate.

- Whichever route fits, compare multiple lenders, review all fees, and choose the option that matches your actual financial situation — not just the lowest advertised rate.