If you are juggling three credit cards, a personal loan, and maybe a consumer durable EMI, you already know the real pain isn't the debt itself — it's tracking five different due dates every month. Miss one, and your credit score takes a hit even if you paid the other four on time.

Debt consolidation solves this specific problem. It doesn't erase what you owe, but it can lower your interest cost and turn a messy juggling act into a single, predictable payment. This guide breaks down how it actually works in India, who qualifies, what it costs, and where people commonly go wrong.

Quick Highlights Table

| Parameter | Typical Range |

|---|---|

| Eligibility | Salaried & self-employed, 21–58 years |

| Minimum Income | ₹15,000–₹25,000/month (varies by lender) |

| Loan Amount | ₹50,000 – ₹40 lakh |

| Interest Rate | 10.5% – 22% p.a. (credit-score dependent) |

| Tenure | 12 – 60 months |

| Documents | KYC, income proof, existing loan statements |

| Processing Time | 24 hours – 7 working days |

Note: These figures are indicative and vary across banks and NBFCs. Always confirm current rates directly with the lender before applying.

What Is Debt Consolidation, Really?

In simple words, debt consolidation means taking one new personal loan to pay off several existing debts — credit card dues, personal loans, or other high-interest borrowings — and then repaying just that one loan.

Think of Rohan, a 32-year-old marketing executive in Pune. He had:

- Credit Card 1: ₹1.2 lakh outstanding at 42% annual interest

- Credit Card 2: ₹80,000 outstanding at 39% annual interest

- A personal loan EMI of ₹6,000/month at 18% interest

Instead of paying three different amounts on three different dates, Rohan took a consolidation loan of ₹2.5 lakh at 13% interest for 3 years. His combined EMI came down, and more importantly, he stopped bleeding money on credit card debt, which is among the costliest borrowing in India.

💡 Expert Insight

Credit card interest in India is calculated monthly and compounds fast — a 3.5% "monthly rate" can translate to well over 40% annually once you account for compounding. This is exactly why moving credit card dues into a lower fixed-rate loan makes mathematical sense for most people.

📌 Did You Know?

RBI data has repeatedly shown that credit card outstanding balances are among the fastest-growing retail credit categories in India, which is one reason lenders now actively design consolidation and balance-transfer products for this exact problem.

Benefits of Low Interest Debt Consolidation

1. One EMI instead of many

You deal with a single lender, single due date, single statement — moving from a multiple-EMI setup to a single EMI loan alone reduces the chance of missed payments.

You deal with a single lender, single due date, single statement — moving from a multiple-EMI setup to a single EMI loan alone reduces the chance of missed payments.

2. Lower overall interest outgo

If your existing debts are at 30–42% (typical for credit cards), moving them to a consolidation loan at 11–16% can cut your interest cost significantly over the loan tenure. Use an EMI calculator to see the exact difference for your numbers.

If your existing debts are at 30–42% (typical for credit cards), moving them to a consolidation loan at 11–16% can cut your interest cost significantly over the loan tenure. Use an EMI calculator to see the exact difference for your numbers.

3. Improved credit utilisation ratio

Once credit cards are paid off through consolidation, your credit utilisation drops, which is one of the factors credit bureaus weigh when calculating your score.

Once credit cards are paid off through consolidation, your credit utilisation drops, which is one of the factors credit bureaus weigh when calculating your score.

4. Predictable budgeting

A fixed EMI over a fixed tenure is easier to plan around than variable minimum-due amounts on multiple cards.

A fixed EMI over a fixed tenure is easier to plan around than variable minimum-due amounts on multiple cards.

5. Reduced collection calls and stress

Multiple lenders following up for payments can be mentally exhausting. Consolidation reduces that to a single point of contact.

Multiple lenders following up for payments can be mentally exhausting. Consolidation reduces that to a single point of contact.

💡 Expert Insight

Consolidation works best when the new interest rate is genuinely lower than the weighted average rate of your existing debts. If a lender offers consolidation at a rate close to what you're already paying, the exercise may not be worth the processing fee.

Eligibility Criteria

| Criteria | Salaried Applicants | Self-Employed Applicants |

|---|---|---|

| Age | 21–58 years | 25–65 years |

| Minimum Monthly Income | ₹15,000–₹25,000 | ₹20,000–₹30,000 (or ITR-based) |

| Work/Business Vintage | 1+ year with current employer | 2–3 years in business |

| Credit Score | 650+ (700+ for best rates) | 650+ (700+ for best rates) |

| Existing Debt Check | Lender reviews current loan/card statements | Lender reviews current loan/card statements |

| Residence | Indian resident | Indian resident |

Salaried applicants can check detailed criteria on our debt consolidation for salaried employees page, or review the full debt consolidation loan eligibility guide before applying.

Disclaimer: Eligibility criteria differ across banks and NBFCs and are subject to internal credit policy, which can change without notice. The figures above are general market indicators, not a guarantee of approval. Please verify exact eligibility with your chosen lender before applying.

📌 Did You Know?

Many lenders now check your existing loan statements not just to verify debt, but to calculate your Fixed Obligation to Income Ratio (FOIR). A FOIR above 50–60% often makes approval harder, regardless of your income level.

Documents Checklist

- PAN Card and Aadhaar Card (KYC)

- Passport-size photograph

- Salary slips (last 3 months) or ITR (last 2 years for self-employed)

- Bank statements (last 6 months)

- Statements of all existing loans/credit cards to be consolidated

- Employment proof or business registration proof

- Address proof (if different from Aadhaar)

💡 Expert Insight

Keep your existing loan closure or foreclosure statements handy. Some lenders disburse the consolidation loan directly to your existing creditors, while others credit it to your account and expect you to close the old debts yourself. Knowing this in advance avoids confusion at disbursal stage.

Interest Rate Comparison: Common Debt Types vs Consolidation Loan

| Debt Type | Typical Interest Rate (Annual) |

|---|---|

| Credit Card Outstanding | 30% – 45% |

| Personal Loan (unsecured, poor credit) | 18% – 26% |

| Consumer Durable EMI (no-cost claims aside) | 15% – 24% |

| Low Interest Debt Consolidation Loan | 10.5% – 16% (score-dependent) |

| Loan Against Property (secured consolidation) | 9% – 13% |

This is why consolidation particularly makes sense for people carrying credit card debt — the interest rate gap is usually the widest here. See current debt consolidation interest rates for the latest lender-wise figures.

📌 Did You Know?

A secured consolidation loan (against property or fixed deposit) usually carries a lower rate than an unsecured one, but it also puts your asset at risk if you default. This trade-off is worth thinking through carefully before choosing the secured route.

How the Process Works

- Check your eligibility and credit score — most lenders offer a free pre-check.

- Apply with your consolidation amount — calculate the total of all debts you want to close, through online debt consolidation services.

- Submit documents — KYC, income proof, and existing loan/card statements.

- Verification and approval — typically 24 hours to 7 working days, or faster with an instant debt consolidation loan.

- Disbursal and closure — either the lender pays your existing creditors directly, or you receive the amount and close the old accounts yourself.

- Start your single new EMI — track this like you would any other loan repayment.

💡 Expert Insight

Always get a written closure confirmation (or a "no dues certificate") from your old lenders after paying them off. Some borrowers assume the debt is closed simply because they've paid, but the account still shows "active" in credit bureau records until the lender formally updates it.

Responsible Borrowing: What to Keep in Mind

Debt consolidation is a tool, not a fix for a spending problem. A few honest cautions worth reading before you apply:

- It only helps if you stop adding new debt. Consolidating your cards and then running up fresh balances on them defeats the entire purpose.

- Check the total cost, not just the EMI. A longer tenure can lower your monthly EMI but increase the total interest paid over time.

- Factor in processing fees and foreclosure charges on your existing loans — these can eat into your savings if not accounted for.

- Don't consolidate if the new rate isn't meaningfully lower. Run the numbers before signing.

- A missed EMI on the new loan affects your score just like any other loan — consolidation doesn't come with extra forgiveness.

📌 Did You Know?

As per RBI's Fair Practices Code, lenders in India are required to disclose the Annual Percentage Rate (APR), not just the flat interest rate, in your loan agreement. Always ask for the APR to understand the true cost of borrowing.

Frequently Asked Questions

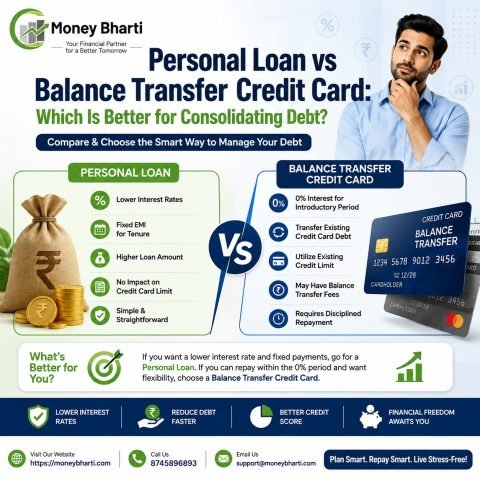

Q1. Is debt consolidation the same as a balance transfer?

Not exactly. A balance transfer loan usually moves one card's dues to another card or lender, often with an introductory low rate. Debt consolidation combines multiple debts — cards, loans, EMIs — into one single loan.

Not exactly. A balance transfer loan usually moves one card's dues to another card or lender, often with an introductory low rate. Debt consolidation combines multiple debts — cards, loans, EMIs — into one single loan.

Q2. Will debt consolidation hurt my credit score?

There may be a small, temporary dip due to the new credit inquiry and account opening. Over time, as your utilisation drops and payments stay consistent, most borrowers see their score improve.

There may be a small, temporary dip due to the new credit inquiry and account opening. Over time, as your utilisation drops and payments stay consistent, most borrowers see their score improve.

Q3. Can I consolidate debt with a low credit score?

It's possible but harder, and the interest rate offered will likely be on the higher end of the range. Some lenders may also ask for a co-applicant or collateral.

It's possible but harder, and the interest rate offered will likely be on the higher end of the range. Some lenders may also ask for a co-applicant or collateral.

Q4. How much can I save by consolidating?

This depends entirely on the interest rate gap between your existing debts and the new loan, and your remaining tenure. Try the debt consolidation EMI calculator before applying.

This depends entirely on the interest rate gap between your existing debts and the new loan, and your remaining tenure. Try the debt consolidation EMI calculator before applying.

Q5. Is a secured consolidation loan always better than unsecured?

Not always. Secured loans usually offer lower rates, but they put your asset (property, FD, gold) at risk. Choose based on your comfort with that risk, not just the rate.

Not always. Secured loans usually offer lower rates, but they put your asset (property, FD, gold) at risk. Choose based on your comfort with that risk, not just the rate.

Final Word

Debt consolidation, done right, is one of the more sensible ways to bring high-interest, scattered debt under control. But it works only when paired with a clear repayment plan and the discipline to not accumulate new debt on the accounts you just paid off. If you're unsure which option fits your situation, it's worth speaking to your bank or a financial advisor before committing to any loan.

This article is for general informational purposes only and does not constitute financial advice. Interest rates, eligibility, and terms mentioned are indicative and subject to change by individual lenders. Please verify current details directly with the lender before applying.