Today, there’s hardly anyone unaware of debt consolidation, especially credit card users. A credit card is easy money. You can use it as you please, but it comes at a high cost in interest. If you fail to return your credit card dues, you will pay a huge interest on the unpaid amount. Since debt consolidation interest rates are much lower than credit card rates, consolidating debt into a single, low-interest loan saves money.

How Debt Consolidation Works?

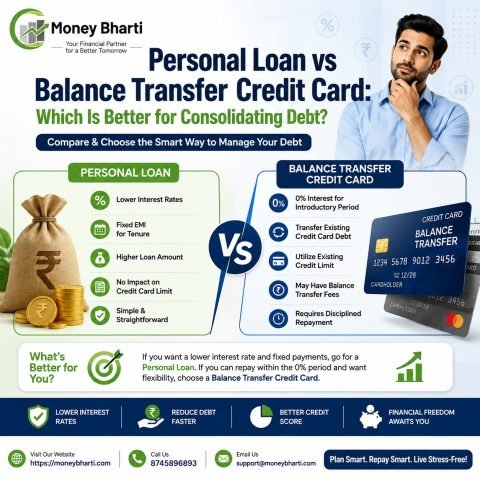

The objective of debt consolidation is to reduce interest rates, and you will be surprised to know that you can reduce your interest rate to almost half after consolidating your debt.

For example:

Interest rates per annum | |

Credit cards | 30% to 48% |

Debt consolidation | 9.99% to 24% |

The comparison table gives a clear view of how much you’re paying on your unpaid credit card dues and how much you can save on consolidating your debt. The savings will increase your cash flow and reduce your credit. In this way, you can become debt-free without liquidating your assets. A hard fact about credit card debt is that most debtors have to liquidate their assets to pay their debt.

What Determines Your Interest Rate?

Low interest is the biggest attraction of a balance transfer loan. The good thing is that you can also get the lowest interest rate on debt consolidation. If you know the important factors that can make you eligible for low interest rates, you can really make a difference to your debt payment. You can save money while paying your debt. In this way, you can keep things simple and affordable.

1. Credit Score

Your credit score is of high interest to lenders. It shows the real picture of your financial history and credit profile. The credit score is divided into the following categories.

- 750 and above: Excellent

- 700-749: Good

- 650-699: Moderate

- Below 650: Average

Check your credit score for free and apply only when it is good. It isn’t that you can’t get a loan with a moderate or average score, but you need an excellent score to qualify for the lowest interest rate. If your credit score is below 650, you need to take steps to strengthen it.

- Pay your bills on time

- Reduce outstanding balance on credit cards

- Get correct credit report

- Avoid applying for new credit cards

2. Income and Employment Stability

A stable income is an assurance that you can comfortably repay your loan. For this reason, most lenders target debt consolidation for salaried employees. However, it doesn’t mean that self-employed individuals or entrepreneurs are ineligible for low-interest loans.

Things you can do to prove employment stability

Salaried Employees: Continue working for your current employer to show consistency in income and employment. Switching jobs frequently doesn’t prove employment stability.

Self-Employed: Prove your income through bank statements. Lenders may require bank statements for the last six months or more.

Entrepreneurs: Get ready with your tax papers to prove you run a legitimate and profitable business. An experienced loan agency can help complete your tax papers.

3. Debt-to-Income Ratio (DTI)

Your DTI is your monthly income after deducting your monthly payments. A low DTI shows you save a sufficient amount to repay a new loan. Conversely, a higher DTI shows you have little amount to repay a new loan. In this situation, lenders will avoid giving a bigger loan. However, you can expect a small loan that you can repay. Increasing your income and debt payment can lower your DTI and make you eligible for a low-interest credit card debt consolidation loan. Your loan agent can suggest more ways to lower your DTI and find a low-interest loan you qualify for.

4. Loan Amount & Tenure

Use an online debt consolidation EMI calculator to calculate your monthly EMI. It will give a fair idea of how much loan you can repay. The good thing is that many lenders offer better interest rates on bigger loans, while others encourage people to borrow smaller loans.

Loan tenure can also help reduce the interest rate. For example, shorter tenure often carries a lower interest rate. When you agree to repay the loan in a short time, you get a rebate on the interest rate. Longer tenures may feel convenient, but they increase the total interest paid over time.

How to Compare Debt Consolidation Interest Rates

Many factors come into play when you compare interest rates on debt consolidation.

Compare the APR

Annual Percentage Rate (APR) gives the right picture of how much you will pay for a loan. It includes:

- Interest rate

- Loan fee

- Lender costs

For this reason, loan agents always consider APR and not just the interest rate.

Hidden Fees

Lenders often add hidden charges in the disguise of various fees. These charges are in addition to the APR.

- Origination fee

- Administration fee

- Late payment charges

- Early payment charges

- Processing fee

Here, you will need the help of an experienced loan agency. Loan agencies work with lenders, and for this reason, they have a better idea of hidden charges.

Compare Total Loan Cost

Multiple EMI to single EMI loan can save you plenty of money on interest, but it can also increase your overall debt payment. A mistake most people make is that they calculate only interest. You should calculate the total amount, including interest, necessary fees, and debt payment, to know how much a loan costs you.

Final Thoughts

Before you accept a loan offer, you should shop around. Here, a loan agent can help. An experienced agent can find the loan you can qualify for. The agent will keep all important factors in mind when suggesting loans. Debt consolidation can save you interest, but you should be eligible for the lowest interest rate.

Your debt consolidation loan eligibility depends on many factors, including your credit score and stable employment. The good thing is that you can improve your eligibility by taking positive steps, like paying your EMIs on time. You can take similar care to get the lowest interest rate.