Credit card debt has a way of growing quietly and then hitting hard. You miss one due date, pay only the minimum, and within a few months the outstanding balance feels impossible to clear — especially when Indian banks charge anywhere between 30% and 45% interest per year on unpaid dues.

The good news is that paying off credit card debt faster isn't about earning more money overnight. It's about picking the right repayment method, negotiating smartly with your bank, and avoiding the traps that keep people stuck in the minimum-due cycle for years.

This guide walks you through exactly how to do that — from the debt avalanche and snowball methods to a debt consolidation loan, balance transfer, and settlement, along with real interest-rate numbers, bank comparisons, and mistakes to avoid.

Quick Answer

To pay off credit card debt faster, stop paying only the minimum due, pick either the avalanche method (highest interest first) or snowball method (smallest balance first), consider a debt consolidation loan or balance transfer to cut your interest rate from 30–45% down to 10–16%, and avoid new spending on the card until the balance is cleared. Borrowers who combine a fixed repayment plan with a lower-interest loan typically clear their debt 40–60% faster than those who keep paying only the minimum.

📌 Need help reducing your debt? Check your instant debt consolidation loan eligibility with Money Bharti.

In This Article

- What is Credit Card Debt Payoff

- How Does It Work

- Top 10 Benefits

- Types of Payoff Methods

- Eligibility

- Documents Required

- Interest Rates Compared

- Bank-Wise Comparison

- Pros & Cons

- Common Mistakes

- Your Payoff Timeline

- Real Example

- FAQs

- Conclusion

📊 India's Credit Card Landscape (2026): Outstanding credit cards in India stood at 119.44 million as of April 2026, up 8.19% year-on-year. Total credit card spending for FY2026 touched ₹23.62 trillion, up nearly 12% from the previous year. With that scale of usage, even a small gap between minimum-due payments and full payoff adds up to a significant national interest bill — and an individual one.

What is Credit Card Debt Payoff?

Credit card debt payoff means clearing your outstanding credit card balance faster than the bank's minimum-due schedule, using a structured method instead of ad-hoc payments.

When you carry forward a balance instead of paying it in full, Indian banks charge interest of roughly 30% to 45% per annum, compounded daily.

Paying only the minimum due (usually 5% of the outstanding amount) keeps the account "current" but barely touches the principal — the rest keeps attracting interest. A payoff strategy replaces this random approach with a fixed plan: a target date, a monthly repayment amount, and a method for deciding which card or loan gets paid first.

How Does It Work?

A credit card payoff plan works by redirecting every extra rupee you can spare toward the debt with the worst terms first, while paying at least the minimum on everything else — this keeps interest from compounding out of control.

Here's the process in practice:

- List every card — outstanding balance, interest rate, and minimum due.

- Choose a method — avalanche (highest rate first) or snowball (smallest balance first).

- Free up monthly cash — trim discretionary spending and redirect it to the target card.

- Consider a lower-interest loan — a personal loan for debt consolidation at 11–16% can replace card debt at 30–45%, turning multiple EMIs into a single EMI.

- Automate payments — set up auto-debit so you never miss a due date and trigger late fees.

- Track progress monthly — check your CIBIL report to confirm balances are dropping and reporting is accurate.

Expert View: "Paying only the minimum due is one of the costliest financial mistakes borrowers make, because most of the payment goes toward interest instead of reducing the principal." — Senior Debt Resolution Analyst, Money Bharti

⚠️ Warning: Never take another credit card to repay an existing one unless you have a proper repayment plan — this often converts one debt into two.

Top 10 Benefits of Paying Off Credit Card Debt Faster

- Lower total interest paid — every month you shave off the timeline saves you 2.5–4% monthly interest.

- Improved CIBIL score — lower credit utilisation boosts your score within 1–2 billing cycles.

- Better loan eligibility — a clean repayment history helps you qualify for home loans and car loans later.

- Reduced financial stress — fewer collection calls and a clear end date.

- Freed-up credit limit — useful for genuine emergencies instead of routine spending.

- Avoids the debt trap — breaks the minimum-due cycle before it becomes unmanageable.

- Protects against rate hikes — banks can revise APR upward on revolving balances.

- Better negotiating position — banks offer better settlement or restructuring terms to proactive borrowers.

- Peace of mind for co-applicants/guarantors — if any card is jointly held.

- More disposable income once cleared — money that went to interest can go to savings or investments.

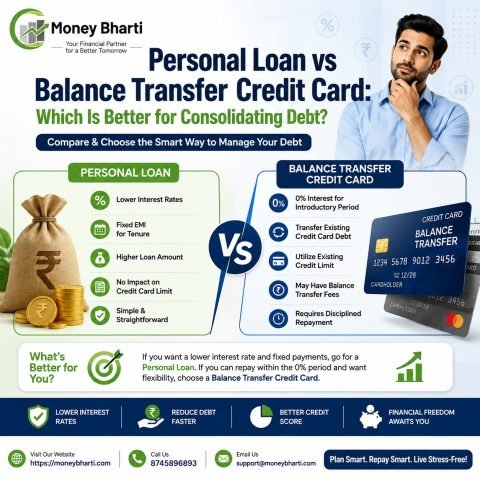

Types of Credit Card Debt Payoff Methods

| Method | How It Works | Best For |

|---|---|---|

| Debt Avalanche | Pay off the card with the highest interest rate first, minimum on rest | Saving the most on interest overall |

| Debt Snowball | Pay off the smallest balance first for quick wins | Staying motivated with multiple cards |

| Debt Consolidation Loan | Take one personal loan to pay off all cards, repay the loan at a lower rate | People juggling multiple EMIs and cards |

| Balance Transfer | Shift outstanding balance to another card with 0% or low introductory rate | Short-term relief on a single large balance |

| Credit Card Settlement | Negotiate a lump-sum payment lower than the total owed | Genuine financial hardship, as a last resort |

These methods aren't mutually exclusive — many borrowers use a consolidation loan for most of the debt and the avalanche method for whatever remains.

Who is Eligible for a Debt Consolidation Loan or Balance Transfer?

Most Indian banks and NBFCs require a CIBIL score of 650 or above, stable monthly income, and at least 6–12 months of credit card repayment history to approve a debt consolidation loan or balance transfer.

Salaried professionals generally have an easier approval path — see this breakdown of debt consolidation for salaried employees for income-specific criteria.

Common eligibility criteria include:

- ✅ Age between 21–60 years

- ✅ Minimum monthly income of ₹15,000–₹25,000 (varies by lender)

- ✅ CIBIL score of 650+ (700+ for the best interest rates)

- ✅ Existing credit card or loan in your name for at least 6 months

- ✅ No ongoing default or written-off account with another lender

Lenders also check your existing debt-to-income ratio before approving a consolidation loan.

Documents Required

- PAN card and Aadhaar card

- Last 3–6 months' bank statements

- Latest credit card statements (all cards you want to consolidate)

- Salary slips (last 3 months) or income proof for self-employed applicants

- CIBIL report (most lenders pull this themselves with your consent)

💡 Before applying, use a debt consolidation EMI calculator to check your projected monthly payment and total interest saved.

Interest Rates Compared

Credit card interest in India typically runs from 30% to 48% per annum, which works out to roughly 2.5% to 4% per month. This is one of the highest borrowing costs available in the retail lending market, which is exactly why replacing it with a lower-rate loan saves so much money. See the full breakdown of current debt consolidation interest rates before you apply.

| Borrowing Option | Typical Interest Rate (Annual) |

|---|---|

| Credit Card (regular purchases) | 30% – 45% |

| Credit Card (cash withdrawal) | 30% – 48% |

| Personal Loan (consolidation) | 10.5% – 18% |

| Balance Transfer (introductory offer) | 0% – 14% for 3–12 months, then standard card rate |

| Gold Loan | 8% – 14% |

| Credit Card Settlement | One-time reduced payout, but credit score impact for up to 7 years |

Bank-Wise Comparison

| Bank/NBFC | Product | Indicative Rate | Notes |

|---|---|---|---|

| SBI | Personal Loan (consolidation) | ~11% – 15% | Lower rate for salaried, government employees |

| HDFC Bank | Balance Transfer + EMI | ~13% – 16% | Processing fee applies |

| ICICI Bank | Personal Loan | ~10.75% – 17% | Faster approval for existing customers |

| Axis Bank | Balance Transfer on Card | Introductory low rate, then standard card APR | Best for short-term relief |

| NBFCs (Bajaj Finserv, etc.) | Personal Loan | ~13% – 24% | Easier approval, higher rate for lower CIBIL |

Rates change frequently — always confirm the current rate directly with the bank before applying.

Pros & Cons

| Method | ✅ Pros | ❌ Cons |

|---|---|---|

| Debt Consolidation Loan | Single fixed EMI, lower interest, predictable end date | Requires decent CIBIL score; processing fee applies |

| Balance Transfer | Quick relief, sometimes 0% for a few months | Interest jumps to standard card rate after the offer period; transfer fee applies |

| Debt Settlement | Immediate reduction in amount owed | CIBIL report shows "Settled" for up to 7 years, affecting future loan approvals |

Common Mistakes to Avoid

- ❌ Paying only the minimum due every month

- ❌ Using the same card for new purchases while repaying old debt

- ❌ Agreeing to a verbal settlement without a written letter from the bank

- ❌ Ignoring the CIBIL report after settlement to confirm correct status update

- ❌ Taking a new loan without comparing rates across at least 2–3 lenders

- ❌ Closing the account before receiving a No Dues Certificate

Expert Tips

✅ Checklist before you start:

- [ ] List all outstanding balances and interest rates

- [ ] Pick avalanche or snowball method and stick to it

- [ ] Set up auto-pay for at least the minimum due on every card

- [ ] Compare 2–3 offers using an online debt consolidation service

- [ ] Get every settlement or restructuring offer in writing

- [ ] Track your CIBIL report monthly until debt is fully cleared

Your Payoff Timeline

| Stage | Milestone |

|---|---|

| Day 1 | Collect all credit card statements and list balances |

| Week 1 | Choose your strategy — avalanche, snowball, or consolidation |

| Month 1 | Start paying extra toward the target debt |

| Month 6 | Outstanding balance visibly lower; CIBIL score starts improving |

| Month 24 | Debt-free (on a typical 2-year consolidation plan) |

Real Example

Rohan, a 32-year-old marketing professional in Pune, was stuck paying only the minimum due on two credit cards. He switched to a consolidation loan and tracked the difference:

| Before | After | |

|---|---|---|

| Outstanding balance | ₹1,80,000 | ₹1,80,000 (consolidated) |

| Interest rate | 42% p.a. | 13% p.a. |

| Monthly payment | ₹9,000 (minimum due) | ₹8,600 (fixed EMI) |

| Time to clear debt | 6–7 years (estimated) | 24 months |

| Total interest paid | — | ₹63,000 saved vs. minimum-due path |

Because the interest rate dropped from 42% to 13%, Rohan cleared the entire debt in two years instead of the 6–7 years it would have taken on the minimum-due path.

Frequently Asked Questions

1. What is the fastest way to pay off credit card debt in India?

Combining the debt avalanche method with a lower-interest consolidation loan is generally the fastest, since it cuts your interest rate from 30–45% down to around 11–16%.

2. Is the debt avalanche or snowball method better?

Avalanche saves more money since it targets the highest interest rate first; snowball keeps you motivated by clearing smaller balances quickly. Either works — the one you'll actually stick to is the "better" one.

3. Can I transfer my credit card balance to another bank?

Yes, most major banks offer balance transfer facilities, often with a low introductory rate for a fixed period before reverting to the standard card rate.

4. Does credit card settlement hurt my CIBIL score?

Yes. A settled account is reported as "Settled" rather than "Closed," and this remains on your credit report for up to seven years, which can affect future loan approvals.

5. What CIBIL score do I need for a debt consolidation loan?

Most lenders prefer a score of 650 or above, with 700+ getting the most competitive interest rates.

6. How much interest do Indian banks charge on credit card debt?

Typically 30% to 48% per annum, or about 2.5% to 4% per month, on the outstanding balance.

7. Can I negotiate my credit card interest rate directly with the bank?

Yes, some banks reduce the rate temporarily for customers with a good repayment history, especially if you ask before missing a payment.

8. What happens if I only pay the minimum due every month?

Your principal reduces very slowly while interest keeps compounding, which can take 5–8 years or more to clear a moderate balance.

9. Is a personal loan better than a balance transfer for paying off credit card debt?

A personal loan usually offers a fixed rate and tenure for the full amount, while a balance transfer often reverts to a high rate after a short introductory period — so a personal loan is generally more predictable for larger debts.

10. What documents are needed for a debt consolidation loan?

PAN card, Aadhaar card, recent bank statements, credit card statements, and income proof such as salary slips.

11. Can I get a No Dues Certificate after settling my credit card?

Yes, banks are required to issue one on request once the settlement amount is paid in full.

12. How long does it take to rebuild my CIBIL score after settlement?

It varies, but consistent on-time payments on a secured card or small loan can show visible improvement within 12–18 months.

13. Are there RBI rules that protect me during debt recovery?

Yes. RBI requires credit card issuers to follow a Fair Practices Code during debt recovery, ensuring respectful and non-coercive interactions — any form of harassment or intimidation during collection is strictly prohibited.

14. Can recovery agents call me at any time?

No — recovery calls are restricted to specific daytime hours, and banks are required to ensure agents follow respectful conduct standards.

15. Should I close my credit card after paying it off?

Not immediately — keeping an old account open (with no balance) can help your credit utilisation ratio and credit history length, unless the annual fee outweighs the benefit.

16. What is the ideal credit utilisation ratio to maintain while repaying debt?

Most experts suggest keeping utilisation below 30% of your total credit limit for the best impact on your CIBIL score.

17. Is paying the minimum due enough to stay debt-free?

No — it keeps your account in good standing but barely reduces the principal, so the balance can take years to clear while interest keeps accumulating.

18. How many years can credit card debt last if I only pay the minimum?

Depending on the balance and rate, it can take anywhere from 5 to 8+ years, and you may end up paying more in interest than the original amount borrowed.

19. Can banks waive credit card interest?

Occasionally, as a goodwill gesture or as part of a settlement or hardship program — but it's not guaranteed and is entirely at the bank's discretion.

20. Can debt consolidation improve my CIBIL score?

Yes, over time — replacing multiple high-utilisation card balances with one fixed-EMI loan lowers your credit utilisation ratio, which is a key scoring factor.

21. What happens if I stop paying my credit card altogether?

The bank will levy late fees and penal interest, report the default to CIBIL (damaging your score for years), and may eventually escalate to recovery agents or legal action.

Conclusion

If you're paying only the minimum due every month, you're likely spending far more on interest than necessary. Review all your credit card balances, compare repayment options, and choose the strategy that best fits your financial situation. Whether it's the avalanche method, a balance transfer, or a debt consolidation loan, taking action early can significantly reduce both repayment time and total interest.

📌 Need help reducing your debt? Check your eligibility with Money Bharti.

External References

- Reserve Bank of India (RBI) — Credit Card Guidelines & Master Direction

- RBI — Banking Ombudsman / Complaint Redressal

- CIBIL — cibil.com

- NPCI — npci.org.in

- National Consumer Helpline — consumerhelpline.gov.in

- Bank-published Fees & Charges / MITC documents (SBI, HDFC Bank, ICICI Bank, Axis Bank)

This article is for general information only and does not constitute financial advice. Interest rates and eligibility criteria are subject to frequent changes — please verify the current terms with your bank or a licensed financial advisor before making a decision.