If you're holding dues on two, three, or even four credit cards, you already know the feeling — different due dates, different minimum payments, and interest quietly piling up on whatever you don't clear each month. A credit card consolidation program is built specifically to fix this: it brings all your card balances together and replaces them with one structured repayment plan.

The term "credit card consolidation program" isn't a single product — it's an umbrella that covers a few different routes, from taking a credit card debt consolidation loan to using a balance transfer or a bank-assisted repayment plan. This guide walks you through each one, in plain language, so you can pick what actually fits your situation.

What is a Credit Card Consolidation Program?

A credit card consolidation program is any structured method of combining multiple credit card balances into a single repayment obligation, usually at a lower or more predictable interest rate than what you're paying across your cards individually. Instead of making three or four minimum payments every month — each barely denting the principal — you make one payment toward one combined balance.

In India, this generally takes one of these forms:

- Debt consolidation loan — a new personal loan that pays off all your card balances at once

- Balance transfer — moving your card dues to another card or lender offering a lower rate

- Bank-assisted repayment or restructuring plan — a structured settlement or extended repayment arrangement offered directly by your card issuer, usually for accounts already overdue

Example: Meera from Chennai has outstanding dues of ₹1,10,000, ₹75,000, and ₹40,000 on three different cards, each charging close to 38%–42% annual interest. She takes a debt consolidation loan of ₹2,25,000 at 14% p.a., which pays off all three cards in full. She now makes a single EMI payment every month, at a fraction of the interest cost she was paying before.

💡 Did You Know?

Credit card interest in India is almost always calculated on a daily reducing balance and compounded monthly, which is why even a "small" unpaid balance can grow surprisingly fast. This is one of the biggest reasons consolidation programs focus on cards first — the interest saved is usually far higher than on any other type of consumer debt.

How It Works

- You list every credit card with an outstanding balance, along with the amount and current interest rate on each.

- You choose a consolidation route — a new loan, a balance transfer, or a bank restructuring plan.

- The chosen lender or issuer verifies your income, credit score, and existing dues.

- On approval, your card balances are paid off directly, and those accounts are closed or brought to zero.

- You now repay only the new consolidated loan or transferred balance, through one EMI or repayment schedule.

Features

- Combines two or more credit card balances into a single repayment obligation

- Typically offered as an unsecured personal loan product, so no collateral is usually required

- Available through banks, NBFCs, and online lending platforms

- Tenure usually ranges from 12 to 60 months, depending on the lender and amount

- Can often be arranged as an instant approval product for well-qualified applicants

- Old card accounts are typically closed or brought to zero balance, freeing up your credit limit

Benefits

- Lower overall interest cost — replacing 36%-42% card rates with a consolidation loan rate can meaningfully cut your total interest outgo.

- Single due date — no more tracking multiple statement dates and minimum due amounts.

- Improved credit utilisation — once card balances are paid off, your utilisation ratio drops, which can help your credit score.

- Clearer payoff timeline — unlike revolving card debt, a consolidation loan has a fixed end date, so you know exactly when you'll be debt-free.

- Less risk of minimum-payment trap — paying only the minimum due on cards keeps you in debt far longer than a structured EMI would.

Eligibility

Check the detailed debt consolidation loan eligibility criteria for your exact profile, since requirements vary by lender. In general, credit card consolidation programs look at:

| Criteria | Typical Requirement |

| Age | 21 to 60 years (varies by lender) |

| Credit Score | Usually 650+ preferred; some NBFCs accept lower scores at higher rates |

| Income | Stable, verifiable income — salaried or self-employed |

| Existing Repayment Record | No major recent defaults, ideally in the last 12 months |

| Number of Cards | Most lenders allow consolidating 2 or more cards in a single loan |

Salaried employees with a steady monthly income generally find it easiest to qualify, though self-employed applicants with clean ITRs are considered too.

⚠️ Eligibility Disclaimer

Final eligibility, interest rate, and loan amount for any credit card consolidation program are decided solely by the respective bank or NBFC after their internal credit assessment. MoneyBharti helps you compare and apply but does not guarantee loan approval.

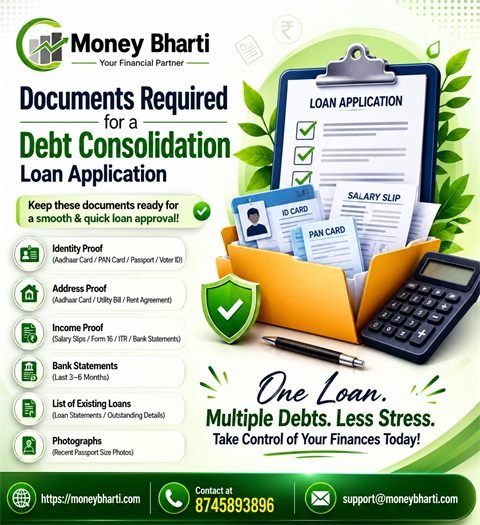

Documents Required

- ✅ PAN Card

- ✅ Aadhaar Card (or other address proof)

- ✅ Latest 3–6 months' bank statements

- ✅ Salary slips (salaried) or ITR for the last 2 years (self-employed)

- ✅ Statements of all credit cards you want to consolidate, showing current outstanding

- ✅ Passport-size photograph

Document requirements may vary slightly between banks, NBFCs, and digital lenders — always check the exact list on the lender's application page before applying.

Interest Rates

Credit card interest rates in India typically range from 30% to 42% per annum when only the minimum due is paid — one of the most expensive forms of consumer debt available. Credit card consolidation loans, by contrast, generally range between 11% and 24% per annum in 2026, depending on your credit score, income, and the lender's assessment. The exact rate you're offered can vary significantly between a bank, an NBFC, and a digital-first lender, so it's worth checking the latest debt consolidation interest rates before committing to one option.

💡 Did You Know?

Moving even one high-interest card balance from a 40% rate to a 14% consolidation loan rate can cut the interest portion of your repayment by more than half over a similar tenure — which is exactly why cards are usually the first thing worth consolidating, before personal loans or other debt.

Processing Charges & Hidden Charges

Most credit card consolidation loans carry a processing fee of around 0.5%–3% of the loan amount, charged upfront or deducted from the disbursed amount. A few lenders run limited-period offers with reduced or waived processing fees, so it's worth comparing a few before applying.

Charges to watch for that aren't always obvious upfront:

- Some card issuers levy a small closure or "no-objection certificate" fee when you pay off and close an account early

- Stamp duty or documentation charges on the new consolidation loan agreement

- Late payment penalties on the new loan if you miss the very first EMI cycle

- GST applicable on processing fees, which can add a small amount to the quoted charge

Step-by-Step Application Process

- List every card and balance — note the outstanding amount and interest rate on each card you want to consolidate.

- Compare lenders — use a platform like MoneyBharti to compare consolidation loan offers suited to your profile.

- Check real savings — run your numbers through our EMI calculator before applying.

- Apply online — fill in your details and upload KYC, income, and card statements.

- Verification and offer — the lender verifies your documents and shares a loan offer with amount, rate, and tenure.

- Disbursal and card payoff — once accepted, the loan amount is used to clear your card balances directly, leaving you with a single EMI going forward.

🧠 Expert Insight

Always confirm with each card issuer that your balance has actually been paid off and the account shows zero outstanding — don't just assume it based on the loan disbursal confirmation. It's common for there to be a small gap between when the loan is disbursed and when it reflects on your card statement, and any leftover balance during that gap can still attract interest.

Approval Timeline

Most banks process a credit card consolidation loan within 3 to 7 working days once documents are submitted and verified. Several online lenders and instant loan platforms can approve and disburse within 24–48 hours for applicants with a strong credit profile and complete documentation.

Pros & Cons

| Pros | Cons |

| Significantly lower interest than typical card rates | Requires a reasonably good credit score to get the best rate |

| One EMI instead of multiple card payments | Processing fees and possible card closure charges add to upfront cost |

| Fixed payoff date, unlike revolving card debt | Doesn't help if your income can't support even a reduced EMI |

| Frees up credit limit once cards are paid off | Risk of running up card balances again if spending habits don't change |

Comparison: Types of Credit Card Consolidation Programs

| Program Type | Best For | Interest Rate Tendency | Key Consideration |

| Credit Card Debt Consolidation Loan | Multiple card balances across issuers | Moderate, often 11%-24% p.a. | Requires credit check and documentation |

| Balance Transfer | A single high-interest card balance | Can be very low or 0% initially | Rate reverts higher after the offer period ends |

| Personal Loan for Consolidation | Combining card dues with other personal debts | Similar to consolidation loan rates | Broader use, not limited to cards only |

| Bank-Assisted Restructuring | Accounts already overdue or in hardship | Varies; may include a reduced settlement amount | Can affect credit report status; lender discretion applies |

Expert Tips

- Consolidate the highest-interest cards first if you're unable to combine everything in one go

- Use the EMI calculator to compare your current total monthly card payments against a proposed consolidation EMI before signing anything

- Ask whether the new lender pays your card issuers directly, or whether you're expected to close the accounts yourself

- Once a card is paid off, consider keeping the account open with a zero balance rather than closing it immediately, since very old accounts can support your credit history length

- Set up auto-debit for your new consolidated EMI so you never miss the very first payment cycle

Common Mistakes

- Consolidating card debt and then using the freed-up credit limit to spend again, ending up with double the debt

- Not comparing multiple lenders and settling for the first consolidation offer received

- Assuming a lower EMI automatically means lower total cost, without checking the tenure and total interest

- Forgetting to confirm that old card balances are actually reduced to zero after the new loan is disbursed

- Ignoring processing fees and card closure charges when comparing the "real" cost of consolidation

Do's & Don'ts

Do's:

- Do list every card balance and interest rate before applying, so you know the true scale of your debt

- Do compare at least 3 lenders on rate, processing fee, and tenure

- Do confirm in writing once each card balance is paid off

- Do set a realistic EMI amount you can comfortably manage every month

Don'ts:

- Don't consolidate and then continue heavy spending on the same cards

- Don't ignore the fine print on processing fees, foreclosure charges, or penal interest

- Don't choose a longer tenure just to get a smaller EMI without checking the total interest paid

- Don't skip comparing offers just because one lender approved you quickly

Myths vs Facts

| Myth | Fact |

| Credit card consolidation always guarantees a lower interest rate | It depends on your credit profile — a strong score gets a meaningfully lower rate, while a weak one may only see a modest difference |

| Consolidation programs are only for people who are already in default | Most consolidation loans are aimed at borrowers who can still repay but want a lower, more manageable rate — not just those in hardship |

| Once I consolidate, my credit score improves immediately | It typically improves gradually, as your utilisation drops and you build a track record of timely EMI payments |

| You can only consolidate cards from the same bank | Most consolidation loans can pay off cards from multiple different banks and issuers in a single loan |

| Consolidation is the same as debt settlement | Consolidation pays off your full debt through a new loan; settlement involves paying a reduced amount and marks the account as "Settled," which affects your credit score |

FAQs

Q1. What is a credit card consolidation program?

It's a structured way to combine multiple credit card balances into a single repayment plan, usually through a consolidation loan, balance transfer, or bank-assisted restructuring.

Q2. How many credit cards can I consolidate at once?

Most lenders allow you to consolidate two or more cards in a single loan, though the exact limit depends on the lender's policy and your total eligible loan amount.

Q3. Will consolidating my credit cards hurt my credit score?

Not if managed well. In fact, paying off high-utilisation card balances and maintaining timely EMI payments on the new loan can improve your score over time.

Q4. Is credit card consolidation the same as a balance transfer?

Not exactly. A balance transfer usually moves one card's balance to another card or lender, while consolidation typically combines multiple cards (and sometimes loans) into a single new loan.

Q5. What interest rate can I expect on a consolidation loan?

In 2026, rates typically range from 11% to 24% per annum, depending on your credit score, income, and the lender's assessment.

Q6. Do I need a good credit score to qualify?

A score of 650 or above is generally preferred, with scores of 700+ usually qualifying for the best rates.

Q7. How fast can a credit card consolidation loan be approved?

Many digital lenders can approve within 24–48 hours for well-qualified applicants, while traditional banks may take 3–7 working days.

Q8. Are there any hidden charges in consolidation programs?

Possible charges include processing fees, card closure fees from your existing issuer, stamp duty on the new loan, and late payment penalties — always ask for a full fee breakup upfront.

Q9. Can self-employed individuals apply for card consolidation?

Yes, provided they can show stable income through ITRs and relevant business documents.

Q10. What happens to my old credit card accounts after consolidation?

They're typically paid off and brought to a zero balance. You can choose to close them or keep them open with no balance, depending on your credit strategy.

Q11. Is it safe to use an online platform to compare consolidation offers?

Yes, as long as you're using a recognised, trusted platform and applying with licensed banks or NBFCs. Always verify the lender's RBI registration before sharing sensitive documents.

Q12. Can I consolidate cards along with a personal loan?

In many cases, yes — a personal loan for debt consolidation can often combine both card dues and existing personal loans into one EMI.

Q13. What if I miss an EMI on my new consolidation loan?

Like any loan, a missed EMI can attract late fees and negatively affect your credit score — only consolidate to an EMI amount you can comfortably manage.

Q14. Does consolidation always save money compared to paying cards individually?

Usually yes, if your card rates are high, but not always — if your existing rates are already low, the savings may be smaller, though repayment still gets simpler.

Q15. Can I consolidate credit card debt more than once?

Yes, but repeated consolidation without changing spending habits usually adds fresh fees each time without solving the underlying issue.

Conclusion

A credit card consolidation program isn't a magic fix — it's a restructuring tool that works best when paired with a genuine change in spending habits. Used well, it can bring down your interest cost significantly, simplify your monthly payments into one predictable EMI, and give you a clear payoff date instead of open-ended revolving debt. Used carelessly — for example, consolidating and then running the same cards back up — it can leave you with more debt than you started with.

If you're juggling dues across multiple credit cards, start by listing every balance and rate honestly, then compare your options: a credit card debt consolidation loan, a balance transfer, or a broader personal loan for consolidation — before committing to one.

Responsible Borrowing Note

This content is meant for general informational purposes and is not financial advice. Loan approval, interest rates, and terms are entirely at the discretion of the respective bank or NBFC based on their credit policy. Please assess your repayment capacity carefully and read all loan terms before signing.