Quick Summary

Before applying for a debt consolidation

loan, understand your financial situation, review your credit score, compare

lenders, calculate your EMI, and read the loan agreement carefully. Avoiding

the common mistakes below can improve your approval chances and reduce your

overall borrowing cost.

Common Mistakes at a Glance

|

Common Mistake

|

Possible Impact

|

How to Avoid It

|

|

Applying without understanding finances

|

Wrong loan amount

|

Review debts and budget

|

|

Not checking credit score

|

Higher rejection risk

|

Check score before applying

|

|

Borrowing more than needed

|

Higher EMI

|

Borrow only required amount

|

|

Ignoring total loan cost

|

Higher overall cost

|

Compare APR and fees

|

|

Applying to multiple lenders

|

Multiple hard enquiries

|

Compare first, apply once

|

|

Not reading agreement

|

Unexpected charges

|

Read all terms

|

|

Choosing only by interest rate

|

Poor overall value

|

Compare all features

|

|

Not comparing offers

|

Miss better deals

|

Compare multiple lenders

|

|

Continuing new debt

|

Debt cycle continues

|

Control unnecessary spending

|

Before You Apply Checklist

·

Know your total outstanding

debt

·

Check your credit score

·

Compare lenders

·

Estimate your EMI

·

Read loan terms

·

Review fees and charges

Debt consolidation is a reliable way to clear debts, especially credit card dues. However, you need to know what to do when applying for a credit card debt consolidation loan. People often make mistakes that make them ineligible for the loan. In this blog, you will learn about the common mistakes to avoid.

1. Applying Without Understanding Your Financial Situation

It is necessary to do your homework before applying for a new loan. If you want to consolidate your debt, you should first determine the following things:

- Total outstanding balance

- Interest rate for each debt

- Minimum monthly payments

- Any late fees or penalties

Having a clear understanding of your finances will help you calculate how much loan you need to clear your dues. You can also calculate your savings on interest rate, loan tenure, and expected EMI for the new loan.

2. Not Checking Your Credit Score

Your debt consolidation loan eligibility largely depends on your credit score. If you don’t check your credit score before applying for a loan, you may face disappointment.

Check your credit score:

- 750 and above: Excellent

- 700-749: Good

- 650-699: Moderate

- Below 650: Average

If your credit score is moderate or average, you have little chance of getting a loan. If you get a loan, it will carry a high interest rate. Reviewing your current credit score is also necessary for the following reasons:

- Identify inaccuracies

- Correct reporting errors

- Improve your credit score before applying

A clear understanding of your credit score can help boost your chances. You will be better prepared to apply for a loan. Lenders will consider your request.

3. Borrowing More Than You Need

A balance transfer loan can ease your financial burden to a large extent. It can make you debt-free in a short time. However, you should avoid applying for a loan that is much greater than your needs. While you may get a big loan, it can increase your repayment obligation and the total cost of the loan. It will be like jumping from one pit to another. You will pay off one debt but will have a new debt to repay.

4. Ignoring the Total Loan Cost

Borrowing a loan will cost you a price. It isn’t only about the interest rate or monthly EMI. It is also about Annual Percentage Rate (APR) and applicable charges. If you don’t calculate the total cost of the loan, you may end up accumulating more debt.

Factors to consider when borrowing a new loan:

- Interest rate

- Annual Percentage Rate (APR)

- Loan tenure

- Monthly EMI

- Total repayable amount

- Applicable fees

Calculating the total cost of a loan can help form an opinion on the loan offer. You can get multiple offers from different lenders and compare their offers to find the best.

5. Applying with Multiple Lenders Simultaneously

Submitting multiple loan applications can result in multiple hard inquiries. It may lower your credit score and reduce your chance of getting a loan. Research lenders, especially their terms and conditions and apply for a multiple EMI to single EMI loan you qualify for. In this way, you can prevent hard inquiries when applying for a loan. Many lenders have prequalification tools that allow potential borrowers to check eligibility before applying. Use these tools instead of applying without knowing about your eligibility.

6. Not Reading the Loan Agreement Carefully

Don’t forget to read the loan agreement carefully before signing. It is an opportunity to clear all your doubts before making any financial commitment to a lender. For this reason, people are advised to seek help from experienced loan agents. They do all the homework before recommending loan offers.

Review before accepting:

- Interest rate details

- Repayment schedule

- Payment due dates

- Fees and penalties

- Default provisions

- Early repayment policies

If you have any queries or doubts regarding any term or condition of the loan, you can ask the lender to clear your doubts before you proceed.

7. Choosing a Loan Based Only on Interest Rate

Important factors to consider:

- Customer support

- Loan flexibility

- Lender reputation

- Repayment flexibility

- Overall loan cost

You will be surprised to know that a higher interest rate with reliable customer support and repayment flexibility is much better than a low interest rate with unreliable customer support. It is better to read reviews to learn more about lenders before forming an opinion of them.

8. Failing to Compare Loan Offers

When you have multiple options, you shouldn’t make a decision without comparing. You should know that the loan terms and conditions are written in fine print. If you don’t read between the lines, you may miss important information and opt for an expensive loan.

Things to compare in loans:

- Interest rate

- Total value of the loan

- Flexibility

- Hidden costs

- Necessary fees

Here, an experienced loan agency can help. Your loan agent can help compare the options. You will be surprised to know that the agent will suggest the best loan options and ensure you qualify for those loans.

9. Continuing to Accumulate New Debt

Loan consolidation helps you become debt-free. If you start taking new loans or use your credit cards for unnecessary expenses, you will again accumulate debt. Debt consolidation works well only when you improve your financial planning. You are in debt because of uncontrolled spending. If you want to consolidate your debt, you should first promise to avoid unnecessary spending.

Final Thoughts

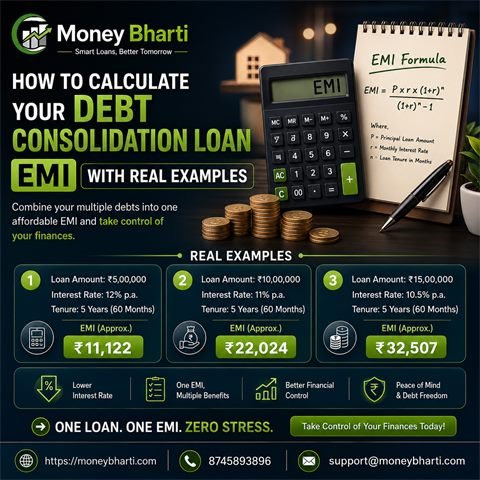

Use an online debt consolidation EMI calculator to calculate the interest rate and EMI of the new loan. It will help you choose the right loan. A loan is an obligation, and if you don’t manage it well, it can put unnecessary pressure on your savings. Debt consolidation can help if you mend your ways. Calculate how much loan you want to become debt-free and the EMI you can pay without feeling any pressure.

Before You Submit Your Application

Before You Submit Your Application

Review your credit score, compare multiple

lenders, calculate your EMI, and borrow only the amount you need. A

well-planned debt consolidation loan can simplify repayments and reduce

financial stress.