Credit card debt has a way of sneaking up on people. You pay the minimum due one month, tell yourself you'll clear it next month, and before you know it, the outstanding balance has grown — quietly, at 30%-42% annual interest — into something that feels impossible to pay off. If that sounds familiar, you're not alone, and more importantly, you have more options than you might think.

"Credit card debt relief" isn't one single product. It's a set of routes — from a straightforward credit card debt consolidation loan to structured repayment plans and, in genuine hardship cases, formal settlement. This guide walks through each option honestly, including what the Reserve Bank of India's rules actually protect you on, so you can choose relief that helps rather than one that quietly makes things worse.

What is Credit Card Debt Relief?

Credit card debt relief refers to any structured method that reduces the burden of your outstanding card dues — either by lowering the interest you pay, combining multiple balances into one manageable payment, or in some cases, negotiating a reduced payoff amount. The right form of relief depends entirely on your situation: whether you can still pay but need a cheaper rate, or whether you genuinely cannot repay the full amount at all.

In India, the main forms of credit card debt relief include:

- Debt consolidation loan — a new loan that pays off all your card balances, leaving you with one lower-interest EMI

- Balance transfer — moving your card balance to another card or lender offering a lower or promotional rate

- EMI conversion — your existing card issuer converts your outstanding bill into fixed instalments

- Bank-assisted restructuring — an extended repayment plan offered by the issuer, usually for accounts already overdue

- Debt settlement — negotiating a reduced lump-sum payoff, generally treated as a last resort due to its long-term credit score impact

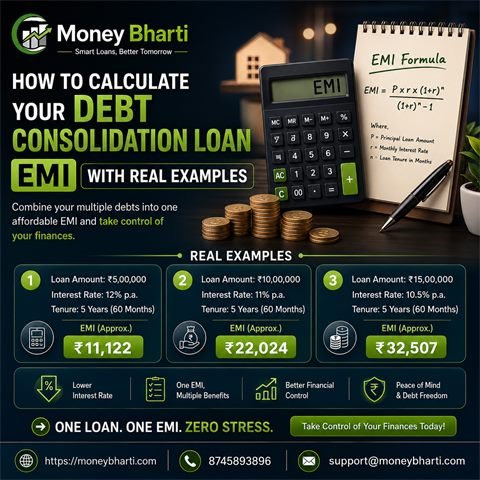

Example: Suresh from Lucknow has ₹2,80,000 spread across two credit cards, both charging close to 40% annual interest after months of paying only the minimum due. He takes a debt consolidation loan at 13.5% p.a., which clears both cards immediately. His EMI is now fixed, predictable, and his total interest cost over the loan tenure is a fraction of what he would have paid continuing on the cards alone.

💡 Did You Know?

As per the Reserve Bank of India's Master Direction on Credit Card and Debit Card Issuance and Conduct, card issuers are required to clearly disclose interest rates, fees, and billing details, and must have a defined process for handling customer grievances. You can read the official guidelines on the RBI website before assuming any relief offer is fair or standard.

How It Works

- You assess your total card debt, including the outstanding amount and interest rate on each card.

- You choose a relief route based on whether you can still make repayments or are facing genuine hardship.

- For consolidation, balance transfer, or EMI conversion — a lender or issuer verifies your details and pays off or restructures your existing balance.

- For restructuring or settlement — you negotiate directly with your card issuer's collections or hardship team.

- You begin repaying under the new, restructured terms, ideally at a lower cost than before.

Features

- Multiple relief routes exist depending on whether you can repay in full or need a reduced payoff

- Consolidation and balance transfer options generally preserve your credit score if repaid on time

- Settlement and hardship restructuring involve a credit report remark that can affect future borrowing

- Most relief options are available through banks, NBFCs, and online lending platforms

- RBI-regulated entities must follow fair practice codes on recovery calls, disclosures, and grievance redressal

Benefits

- Lower interest burden — moving from card rates of 30%-42% to a consolidation loan rate can significantly cut your total interest.

- One manageable payment — instead of tracking multiple due dates, you deal with a single EMI or plan.

- Reduced stress and recovery pressure — a structured plan stops the constant cycle of late fees and collection calls.

- Protected or improving credit score — options like consolidation and balance transfer, if repaid on time, can actually help your credit profile.

- A clear end date — unlike revolving card debt, most relief options give you a fixed payoff timeline.

Eligibility

Eligibility depends on which relief route you're considering. Check the full debt consolidation loan eligibility criteria for consolidation-based relief. In general:

| Relief Option | Typical Eligibility |

| Debt Consolidation Loan | Credit score 650+, stable income, minimal recent defaults |

| Balance Transfer | Reasonable credit score, active card in good standing |

| EMI Conversion | Existing cardholder with eligible outstanding balance — minimal checks |

| Settlement / Restructuring | Genuine financial hardship, account usually overdue; lender discretion applies |

This works well for salaried employees with a steady income who are struggling with high card interest, as well as self-employed individuals who can demonstrate consistent income through ITRs.

⚠️ Eligibility Disclaimer

Final eligibility, interest rate, and approval for any credit card debt relief option are decided solely by the respective bank or NBFC, based on their internal credit policy and RBI-mandated fair practice norms. MoneyBharti helps you compare and apply but does not guarantee approval.

Documents Required

- ✅ PAN Card and Aadhaar Card

- ✅ Latest 3–6 months' bank statements

- ✅ Salary slips (salaried) or ITR for the last 2 years (self-employed)

- ✅ Statements of all credit cards showing current outstanding

- ✅ Proof of financial hardship, if applying for settlement or restructuring (job loss letter, medical bills, income drop proof)

Interest Rates & Charges

Credit card interest in India typically ranges from 30% to 42% per annum when only the minimum due is paid, making it one of the costliest forms of consumer debt. Debt consolidation loans, by comparison, generally range from 11% to 24% per annum in 2026, depending on your credit score and lender. Check current rates on our interest rates page before applying.

Processing fees on consolidation loans usually run 0.5%–3% of the loan amount. Settlement routes typically don't have an "interest rate" as such, but settlement agencies may charge 10%–20% of the settled amount as a fee, and penal interest keeps accruing on your card until a settlement is finalised. Always ask for a complete, written fee breakup before agreeing to any relief plan.

💡 Did You Know?

Under RBI's Integrated Ombudsman Scheme, you can file a free complaint against a bank or NBFC if you believe you've been treated unfairly during recovery or misled about a debt relief offer. Details and the complaint process are available on the RBI Ombudsman portal.

Step-by-Step Process

- List every card balance — note the outstanding amount and interest rate on each card.

- Decide your situation honestly — can you still make repayments at a lower rate, or is full repayment genuinely not possible?

- Compare relief options — a consolidation loan, balance transfer, or EMI conversion for those who can pay; restructuring or settlement discussions for genuine hardship.

- Apply or negotiate — apply online for a consolidation loan, or contact your card issuer's hardship team directly for restructuring.

- Get everything in writing — final terms, rates, and any settlement agreement should be confirmed in writing before you pay anything.

- Follow through consistently — stick to the new EMI or payment plan to actually get the credit score and financial benefit of the relief option.

🧠 Expert Insight

Before assuming settlement is your only option, always check if you qualify for a consolidation loan or balance transfer first — even a partial income can often support a restructured EMI at a much lower rate, without the long-term credit score damage that comes with a "Settled" remark. Relief that keeps your account in good standing is almost always worth more than relief that closes it early.

Approval Timeline

- Debt Consolidation Loan / Balance Transfer: 24 hours to 7 working days with most lenders, with several instant loan platforms approving within 24–48 hours.

- EMI Conversion: Instant to a few hours, since it's processed on your existing card.

- Settlement / Restructuring: Anywhere from a few weeks to a few months, depending on negotiation and lender discretion.

Pros & Cons

| Option | Pros | Cons |

| Consolidation Loan | Lower rate, full payoff, credit score protected | Needs decent credit score and documentation |

| Balance Transfer | Can offer very low or 0% promotional rate | Rate reverts higher after offer period |

| EMI Conversion | Instant, no fresh credit check | Fixes only one card; other dues untouched |

| Settlement | Genuine relief when repayment is impossible | Sharp, long-term credit score damage |

Comparison Table: Credit Card Debt Relief Options

| Parameter | Consolidation Loan | Balance Transfer | Settlement |

| Best for | Multiple cards, stable income | Single high-interest card | Genuine inability to repay |

| Interest Rate | 11%-24% p.a. | 0% initially, then standard rate | No rate — reduced lump sum instead |

| Credit Score Impact | Neutral to positive | Neutral to positive | Sharp negative impact |

| Approval Time | 24 hrs–7 days | 24 hrs–7 days | Weeks to months |

Expert Tips

- Always calculate your total card debt and blended interest rate before choosing a relief option

- Use our EMI calculator to compare your current card payments against a proposed consolidation EMI

- Read RBI's fair practice guidelines on the official RBI website so you know what recovery agents can and cannot legally do

- Treat settlement as a last resort — explore consolidation or restructuring first wherever possible

- Keep every payment receipt, settlement letter, and No Dues Certificate safely for future reference

Common Mistakes

- Waiting too long to seek relief, letting penal interest and late fees pile up before taking action

- Assuming settlement has no credit score impact, when it does — for several years

- Paying an unregulated settlement "agency" an upfront fee without verifying their track record

- Consolidating debt and then running up the same cards again

- Not reading the full terms of a restructuring or settlement offer before agreeing to it

Do's & Don'ts

Do's:

- Do compare consolidation, balance transfer, and restructuring before considering settlement

- Do check your credit report and score before applying for any relief option

- Do get every relief agreement confirmed in writing

- Do know your rights under RBI's Ombudsman Scheme if you feel treated unfairly

Don'ts:

- Don't ignore your card issuer's calls and letters — early communication makes negotiation easier

- Don't sign a settlement or restructuring agreement without reading every clause

- Don't assume all "debt relief" agencies are equally trustworthy — verify before paying any fee

- Don't take on new credit immediately after getting relief on existing debt

Myths vs Facts

| Myth | Fact |

| All credit card debt relief options hurt your credit score | Consolidation loans and balance transfers, if repaid on time, generally protect or even improve your score — only settlement carries a sharp negative impact |

| Banks will never negotiate on credit card dues | Many banks do offer restructuring or hardship plans, especially when you proactively reach out before defaulting |

| Debt relief agencies are regulated the same way as banks | Not all are — always verify a firm's credentials and avoid anyone demanding a large upfront fee before any real negotiation |

| Once you're in card debt, there's nothing RBI can do to help | RBI's fair practice codes and Ombudsman Scheme exist specifically to protect borrowers from unfair recovery practices and misleading offers |

| Consolidation and settlement are the same thing | Consolidation pays off your full debt through a new loan at a lower rate; settlement involves paying less than you owe and marks your account as "Settled" |

FAQs

Q1. What is the fastest way to get credit card debt relief in India?

A debt consolidation loan or balance transfer is usually the fastest route if you can still make repayments, often approved within 24 hours to 7 working days.

Q2. Does credit card debt relief always hurt my credit score?

No. Consolidation loans and balance transfers, when repaid on time, generally protect or improve your score. Only settlement typically causes a sharp, long-term negative impact.

Q3. Can I negotiate directly with my bank for relief?

Yes, many banks offer restructuring or hardship plans if you reach out proactively, especially before your account becomes seriously overdue.

Q4. What does RBI say about credit card recovery practices?

RBI's fair practice guidelines require lenders to follow proper disclosure and grievance redressal processes, and prohibit harassment during recovery. Details are available on the RBI website.

Q5. Is debt consolidation better than settlement?

In almost every case where you can still make some repayment, yes — consolidation protects your credit score, while settlement damages it for years.

Q6. How much interest can I save through consolidation?

Moving from a 35%-40% card rate to a 12%-14% consolidation loan rate can cut your interest cost substantially — use an EMI calculator to check your exact numbers.

Q7. Can I get relief on multiple credit cards at once?

Yes, most consolidation loans are designed to pay off two or more cards simultaneously with a single new loan.

Q8. Where can I file a complaint if I feel a bank treated me unfairly?

You can file a free complaint through RBI's Integrated Ombudsman Scheme at cms.rbi.org.in.

Q9. Is EMI conversion a form of debt relief?

It's a mild form of relief, since it fixes your rate and tenure on one card, but it doesn't address balances on other cards or loans.

Q10. What documents do I need for credit card debt relief?

Typically PAN, Aadhaar, bank statements, income proof, and existing card statements. Settlement or restructuring may also need proof of financial hardship.

Q11. Can self-employed individuals apply for consolidation-based relief?

Yes, provided they can show stable income through ITRs and relevant business documents.

Q12. How long does a settlement negotiation usually take?

It can take anywhere from a few weeks to several months, depending on the lender and how firmly they hold their negotiating position.

Q13. Is the amount waived in a settlement taxable?

It can be treated as income under certain tax rules — it's best to consult a chartered accountant for your specific case.

Q14. Will taking debt relief affect my ability to get a loan in the future?

Consolidation and balance transfer, repaid on time, generally don't hurt future borrowing. Settlement, on the other hand, can make future loan approvals harder for several years.

Q15. What's the safest way to choose a debt relief provider?

Stick to recognised banks, NBFCs, or trusted comparison platforms, verify their RBI registration, and never pay a large upfront fee before any real negotiation has happened.

Conclusion

Credit card debt relief isn't a single fix — it's a range of options, from consolidation loans and balance transfers to restructuring and, as a last resort, settlement. The right choice depends entirely on whether you can still manage repayments or are facing genuine financial hardship. In most cases, options that keep your account in good standing — like a credit card debt consolidation loan — protect your credit score far better than settlement, and cost you less in the long run.

Before choosing any relief option, review your total debt honestly, check your eligibility, and don't hesitate to use RBI's official channels if you ever feel a lender is treating you unfairly during the process.

Responsible Borrowing Note

This content is meant for general informational purposes and is not financial or legal advice. Loan approval, interest rates, and relief terms are entirely at the discretion of the respective bank or NBFC. Please assess your repayment capacity carefully, read all terms before signing, and consult a certified financial advisor if you're unsure which option suits your situation.