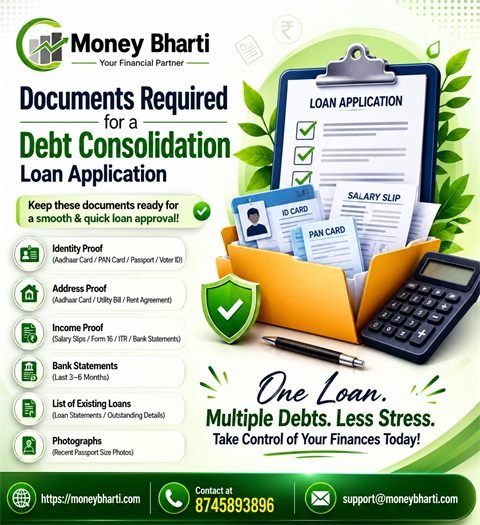

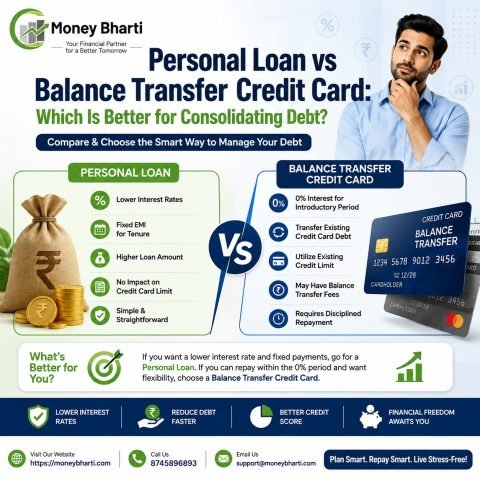

If you are under a heavy debt, consider consolidating your debt into a single, low-interest credit card debt consolidation loan. The objective is to accumulate all your debt in a loan and get some relief from mounting debt. If you are new to debt consolidation, this blog will help you understand the concept and its benefits. You will need a high credit score and stable income to become eligible for a low-interest loan.

What is Debt Consolidation?

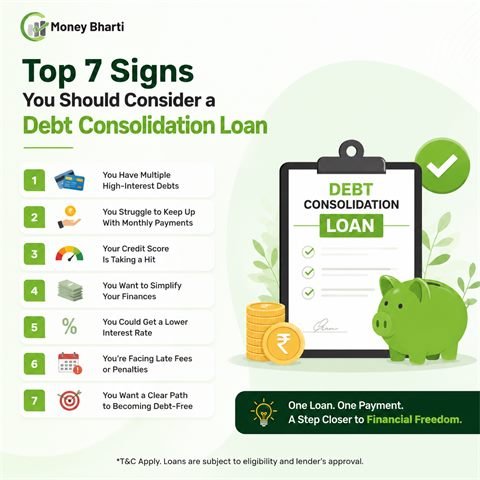

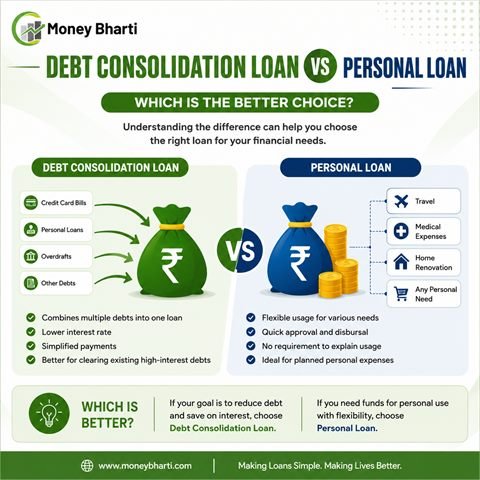

Simply put, it is a financial tool to reduce your debt. For example, if you use multiple credit cards and pay for each card, you pay for three unsecured personal loans that carry a high interest rate. If you consolidate the dues of all credit cards into a single loan, you will have only one loan to repay. The new loan will reduce your interest rate, EMI, and tenure. You can become debt-free within a couple of months or years.

How Debt Consolidation Works?

Debt consolidation interest rates make things simple and affordable for debtors. The problem you are facing isn’t about debt, but the interest rate. You pay a high interest on credit card dues. It is what prevents you from increasing the loan repayment. A large part of your EMI goes to paying interest. When you consolidate your debt, you get a rebate on the interest rate. It not only increases your loan repayment, but also your cash flow. You can choose a loan tenure and become debt-free in a time-bound manner.

Let’s understand debt consolidation with an example

Rahul has accrued a huge debt by using multiple credit cards. Now he wants to consolidate the debt to reduce his financial burden.

Let’s calculate his present interest rate

Credit Card | Total Amount | Interest Rate 40% | GST | Total Interest |

First | 50000 | 1643.84 | 295.89 | 1939.73 |

Second | 75000 | 2465.75 | 443.83 | 2909.58 |

Third | 85000 | 2794.52 | 503.01 | 3297.53 |

Rahul pays a total interest of: 8164.84

It is the minimum amount Rahul pays every month to his credit card companies. You can see it is a huge amount that is putting unnecessary pressure on his finances.

Let’s check how much Raul can save with a balance transfer loan

Total Debt: 2,10,000

Interest rate of new loan: 20%

Total interest paid: 3452.05

GST: 621.37

Total: 3452.05 + 621.37 = 4073.42

Let’s see how much Raul saves by consolidating his debt

Interest paid before debt consolidation = 8164.84

Interest paid after debt consolidation + 4073.42

Total Benefit = 8164.84 – 4073.42 = 4091.42

You can see that Rahul saves almost half the amount he pays for his credit card dues. The saved amount increases his cash flow and helps him become debt-free. The above calculation shows that debt consolidation can free up your finances from the clutches of credit card companies.

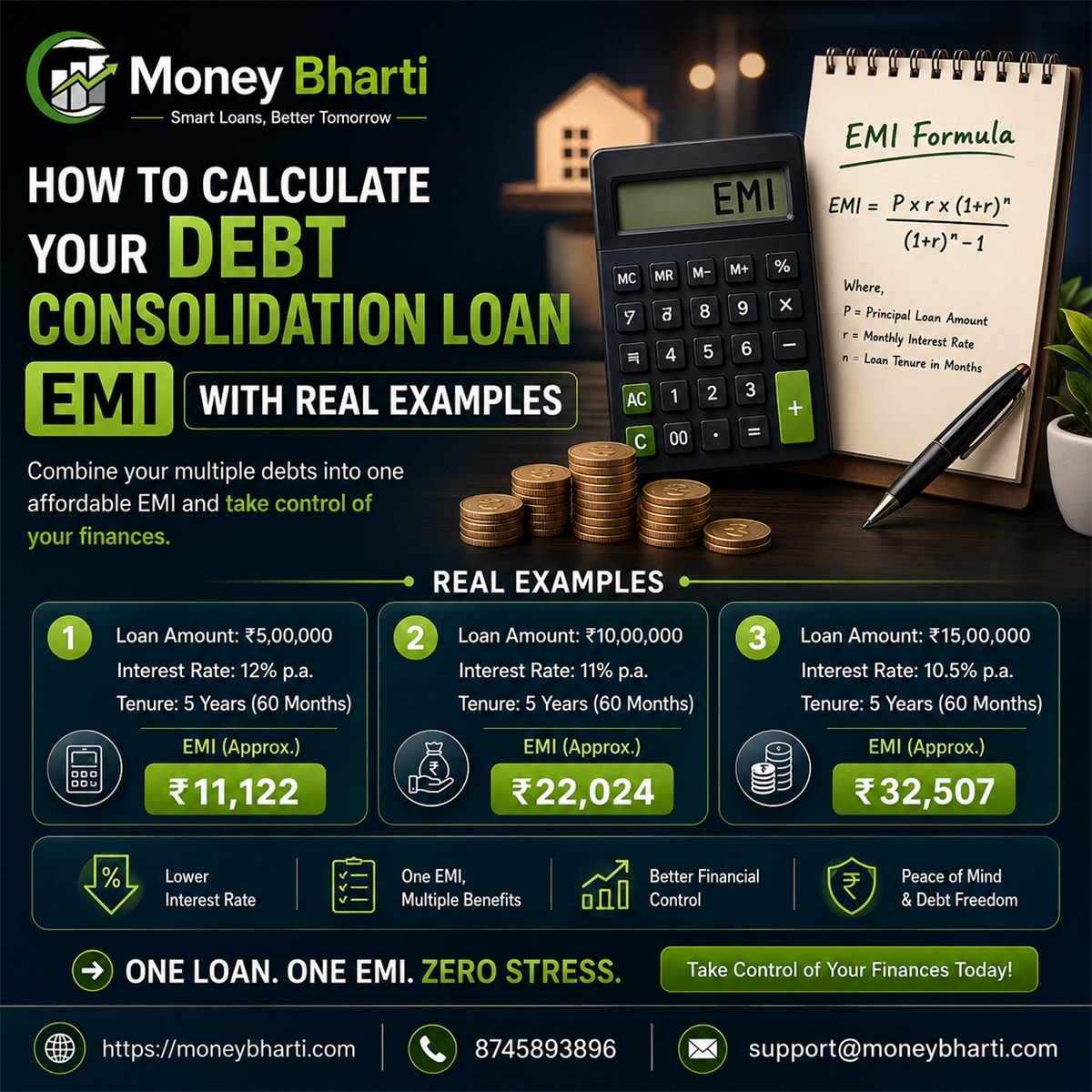

How to calculate the interest rate of debt consolidation loans

You can use an online debt consolidation EMI calculator to calculate the interest rate on your loan. If you want to know how lenders decide the interest rate for debt consolidation loans, you need to learn about the eligibility criteria for low-interest loans. Lenders look into many factors before making any offer.

Your interest rate may differ from what your friends get. Interest rate is decided on a case-by-case basis. If you fulfil their requirements, you may get the lowest interest rate. However, lenders generally offer up to a 20% interest rate. It is still much lower than the interest credit companies charge.

Factors that Affect Interest Rate

1. Credit Score

It is the biggest factor to consider. If you check your current credit score, it will fall into one of the following:

750 and above: Excellent

700-749: Good

650-699: Moderate

Below 650: Average

If your credit score is excellent, you can easily get the lowest interest rate. If it is good, you may have to settle for a slightly higher interest rate. If it is moderate or average, you may be disqualified from a low interest rate. Check your credit score and look for ways to improve it if it is low.

2. Stable Income

It is also an important factor in deciding debt consolidation loan eligibility. If you earn a stable income, such as a salary, you are most likely to receive a lower interest rate. If you are a self-employed person, you need to prove you have a stable job and income. If you do business, you need to submit your tax papers to prove your income. Lenders want to know whether you are capable of repaying a new loan. If they are satisfied, they will offer you a new loan. You can pay off your debts with a new loan and repay the loan.

3. Loan amount & Tenure

Shorter loans often carry a low interest rate, while the interest rate on bigger loans may be slightly higher. Similarly, a shorter tenure can save you some interest. For this reason, people are advised to keep their loan tenures shorter. Short tenure increases EMI, but it provides lasting relief from long-term fatigue. It also reduces the total loan amount. If you want to consolidate your debt, you should borrow as much as needed and keep the tenure shorter for long-term benefits. If you have any doubts, you can discuss your needs with an experienced loan agency.

4. Debt-to-Income Ratio

If your debt is greater than your income, you are in big trouble. If your DTI is high, it means you pay a huge amount of your income in debt settlement. In this situation, you won’t get any benefit from lenders. It is better to look for ways to reduce your DTI. Your loan agent can help strengthen your DTI and enhance your eligibility for a new loan.

Final Thoughts

A multiple EMI to single EMI loan can reduce your financial burden if you can get it. If you fulfil the requirements, you can easily get a new loan to pay off your debts. However, you need a strategy to apply for a new loan. It is better to work with an experienced loan agency that can find the loan you qualify for.