Rohan, a 32-year-old marketing executive in Pune, was paying five different EMIs every month — two credit cards, one personal loan from HDFC, one consumer durable loan for his fridge, and a small NBFC loan he took during a medical emergency.

His total outgo? Nearly ₹42,000 a month, spread across five due dates, five customer care numbers, and five different interest rates — some as high as 42% annually on credit card revolving credit.

He wasn't missing payments. He was just tired of tracking them.

This is where debt consolidation comes in. It's not a loophole, and it's not "free money." It's simply a way to combine multiple debts into one loan, with one EMI, one due date, and — if you pick the right lender — one lower interest rate. If you want the short version, this is essentially a multiple EMI to single EMI loan — one of the most searched solutions for exactly Rohan's kind of problem.

In this guide, we'll walk through the best debt consolidation companies operating in India in 2026, how the process actually works, what it costs, and the mistakes that trip up most first-time applicants. No sales pitch. Just the facts you need before you sign anything.

What is Debt Consolidation?

Debt consolidation means taking one new loan to pay off several existing debts — credit cards, personal loans, and other unsecured borrowings — so you're left with just one EMI instead of many.

Think of it like this: instead of paying rent to five different landlords every month, you take one bigger loan, clear all five payments at once, and then repay just that one loan going forward.

In India, debt consolidation usually happens through:

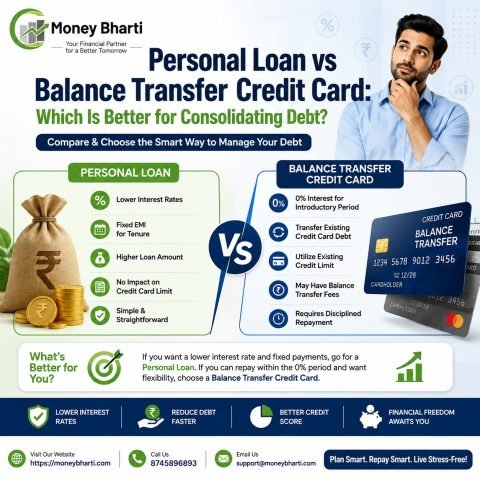

- Personal loans for debt consolidation offered by banks and NBFCs

- Balance transfer loans that shift high-interest card or loan debt to a lower-rate account

- Loan against property (LAP) for those with larger debt amounts and property to pledge

- Debt consolidation programs by fintech NBFCs like CASHe, MoneyTap, or KreditBee for smaller amounts

Read our full breakdown of the debt consolidation loan process if you want to go deeper before applying.

It's important to understand — India doesn't have "debt settlement companies" in the same way the US does, where a third party negotiates with creditors to reduce your total debt. In India, most "debt consolidation companies" are actually lenders giving you a new loan, not agencies negotiating with your existing lenders.

How It Works

Here's the actual flow, step by step:

- You list out all your debts — credit card outstanding, personal loan balances, and their respective interest rates.

- A lender evaluates your total debt and your repayment capacity (based on income and credit score).

- The lender approves a new loan large enough to cover your existing debts.

- The loan amount is disbursed — either directly to your old lenders or to your bank account, which you then use to close the old accounts.

- You get closure letters/NOCs from your previous lenders confirming the debt is paid off.

- You now pay just one EMI to the new lender, ideally at a lower interest rate than your average previous rate.

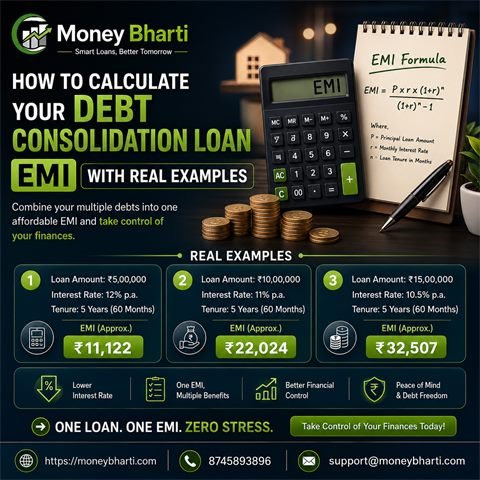

Example: Priya from Bengaluru had ₹3.5 lakh spread across two credit cards (36% and 42% p.a.) and a personal loan (18% p.a.). She consolidated everything into one personal loan at 14% p.a. from a bank, dropping her monthly outflow from ₹19,800 to ₹12,400 — a saving of over ₹7,000 every month.

Features

- Single EMI replacing multiple monthly payments

- Fixed tenure, usually 12 to 60 months

- Interest rates typically lower than credit card revolving rates

- Available as secured (against property/FD) or unsecured loans

- Online application with e-KYC in most cases

- Pre-closure and part-payment options with select lenders

- Loan amounts ranging from ₹50,000 to ₹40 lakh depending on the lender and your profile

- Some NBFCs offer top-up facility after 6–12 months of clean repayment

Benefits

- One EMI, one date — no more tracking five due dates

- Lower overall interest — replacing 36–42% credit card rates with 11–18% personal loan rates

- Improved credit score over time — timely repayment of one consolidated loan reflects better than multiple accounts with high utilisation

- Reduced mental stress — genuinely underrated, but real. Fewer calls from recovery agents, fewer things to remember

- Better cash flow planning — a fixed EMI is easier to budget around than variable credit card minimum payments

- Possible negotiation room — some banks offer relationship-based rate discounts if you're an existing customer

Eligibility

Most Indian lenders look at similar criteria, though exact numbers vary:

- Age: 21 to 60 years (salaried) or up to 65 (self-employed)

- Minimum income: ₹20,000–₹25,000/month for metro cities; ₹15,000 for smaller towns (varies by lender)

- Credit score: 650+ preferred; 700+ gets you the best rates

- Employment: Salaried with at least 1–2 years of work experience, or self-employed with 2+ years of business continuity

- Existing debt-to-income ratio: Most lenders want your total EMIs (including the new one) to stay under 50–55% of monthly income

Important: If your credit score has already dropped below 600 due to missed payments, many mainstream banks will reject you. This is where NBFCs (at slightly higher rates) or a co-applicant become useful.

For a full breakdown of criteria by lender, check our detailed debt consolidation loan eligibility page. If you're a salaried applicant, our debt consolidation for salaried employees guide covers salary-slab-wise offers from major banks.

Required Documents

For salaried applicants:

- PAN card and Aadhaar card

- Last 3 months' salary slips

- Last 6 months' bank statement

- Form 16 or latest ITR (some lenders ask)

- Employee ID card / offer letter (for newer employees)

For self-employed applicants:

- PAN card and Aadhaar card

- Business registration proof (GST certificate, shop license, etc.)

- Last 2 years' ITR with computation of income

- Last 6–12 months' bank statement (business account)

- Profit & Loss statement, audited if turnover crosses the threshold

For all applicants (debt consolidation specific):

- Statement of all existing loans/credit cards to be consolidated

- Foreclosure/outstanding letters from current lenders

- Passport-size photographs

Interest Rates

Rates change with RBI's repo rate movements, so always confirm current rates directly with the lender before applying. As a general 2026 market range:

Lender Type | Approx. Interest Rate (p.a.) |

| Public sector banks (SBI, PNB, BoB) | 10.5% – 15% |

| Private banks (HDFC, ICICI, Axis) | 10.75% – 18% |

| NBFCs (Bajaj Finserv, Tata Capital, IIFL) | 12% – 24% |

| Digital-first NBFCs (MoneyTap, CASHe, KreditBee) | 18% – 36% |

| Loan against property | 9% – 13% |

Rule of thumb: If your average existing debt interest rate is above 20%, almost any of these options will save you money. If it's already below 14%, consolidation may not help much — do the math before switching.

For live, lender-wise numbers, see our updated debt consolidation interest rates page — rates here change with RBI's repo rate, so we refresh it regularly.

Processing Charges

- Banks: Usually 0.5% to 2% of the loan amount, often with a cap (e.g., max ₹10,000–₹15,000)

- NBFCs: Typically 2% to 4%, sometimes higher for smaller-ticket loans

- GST: 18% is charged additionally on the processing fee itself

- Some lenders run festive offers (Diwali, New Year) waiving processing fees partially — worth checking before you commit

Example: On a ₹5 lakh consolidation loan at 2.5% processing fee + 18% GST, you'd pay roughly ₹14,750 upfront — factor this into your savings calculation.

Hidden Charges (if applicable)

These are the ones people miss, and they matter:

- Prepayment/foreclosure charges: 2–5% of outstanding principal if you close the loan early (floating rate personal loans to individuals are usually exempt under RBI rules, but always confirm in writing)

- Bounce charges: ₹400–₹750 per failed EMI, plus possible late payment interest

- Loan cancellation fee: If you back out after disbursal, some lenders charge a cancellation fee

- Stamp duty: Varies by state, usually deducted from the disbursed amount

- Insurance bundling: Some lenders push a loan protection insurance policy at disbursal — it's usually optional, not mandatory. Ask directly and get it removed if you don't want it.

- Documentation/legal fee: More common in secured loans like loan against property

Step-by-Step Application Process

- List your existing debts with exact outstanding amounts and interest rates

- Check your credit score (CIBIL, Experian, or Equifax) — this decides which lenders you qualify for

- Compare 3–4 lenders on rate, processing fee, and tenure flexibility (use the comparison table below). Run the numbers on our debt consolidation EMI calculator before deciding

- Apply online or via branch with your basic KYC and income documents — most lenders now support fully online debt consolidation services with e-KYC

- Get a sanction letter stating the approved amount, rate, and tenure

- Verify disbursal method — direct payoff to old lenders vs. amount credited to your account

- Close old accounts and collect NOC/closure certificates — don't skip this step

- Update your credit report — request old lenders to report "closed" status within 30–45 days

- Set up auto-debit (NACH/ECS) for the new EMI to avoid missed payments

Approval Timeline

Stage | Typical Time |

| Online application submission | 10–15 minutes |

| Document verification | 1–2 working days |

| Credit check & approval | 1–3 working days |

| Disbursal after approval | Same day to 2 working days |

| Total (pre-approved customers) | Few hours to 1 day |

| Total (new-to-bank applicants) | 3–7 working days |

NBFCs and digital lenders are usually faster (often same-day) but at a higher interest cost. Banks take a bit longer but generally offer better long-term rates. If speed matters more than rate for your situation, compare options on our instant debt consolidation loan page.

Pros & Cons

Pros:

- Simplifies multiple payments into one

- Can meaningfully reduce total interest paid

- Improves credit utilisation ratio once cards are closed

- Easier to budget with a fixed EMI

- Reduces the chance of accidentally missing a payment

Cons:

- Doesn't work if your new rate isn't actually lower than your blended old rate

- Processing fees and possible foreclosure charges eat into savings

- Risk of running up credit card debt again if the old cards stay open and active

- Longer tenure can mean paying more total interest even at a lower rate — always check the total repayment amount, not just the EMI

- Rejected applications get logged as credit inquiries, which can temporarily dip your score

Comparison Table

Lender | Interest Rate (p.a.)* | Max Loan Amount | Processing Fee | Approval Time |

| SBI Personal Loan | 10.5% – 14% | Up to ₹20 lakh | Up to 1.5% | 2–5 days |

| HDFC Bank Personal Loan | 10.75% – 16% | Up to ₹40 lakh | Up to 2.5% | 1–3 days |

| ICICI Bank Personal Loan | 10.85% – 16.5% | Up to ₹25 lakh | Up to 2.5% | 1–3 days |

| Axis Bank Personal Loan | 11% – 17% | Up to ₹40 lakh | Up to 2% | 2–4 days |

| Bajaj Finserv Personal Loan | 11% – 24% | Up to ₹55 lakh | Up to 4% | Same day–2 days |

| Tata Capital Personal Loan | 11.5% – 19% | Up to ₹35 lakh | Up to 3% | 1–2 days |

| MoneyTap (App-based credit line) | 13% – 36% | Up to ₹5 lakh | Up to 2% | Instant–1 day |

Rates are indicative for 2026 and change with RBI policy, applicant profile, and lender offers. Always check the live rate on the lender's official page before applying.

Expert Tips

- Calculate the "true cost," not just the EMI. A lower EMI over a longer tenure can cost more overall. Compare total interest payable, not monthly comfort.

- Close old cards, don't just clear them. If you pay off a credit card but keep it open with a high limit, the temptation to reuse it is real — and common.

- Negotiate with your existing bank first. If you already have a salary account or FD with a bank, ask about a top-up or balance transfer before shopping elsewhere — existing customers often get preferential rates.

- Avoid stacking a consolidation loan on top of unresolved debt. If you consolidate but keep borrowing on other cards, you'll end up worse off within a year.

- Time it with your credit score check. Apply when your score is at its best — even a 20-point difference can shift your interest rate by 1–2%.

- Read the foreclosure clause before signing. Ask specifically: "Can I close this loan early, and what will it cost me?"

Common Mistakes

- Consolidating debt without cutting up or freezing the old credit cards

- Choosing the lender with the lowest EMI without checking the tenure or total interest

- Not getting closure letters/NOCs from old lenders after payoff

- Ignoring processing fees and GST while comparing "cheapest" options

- Applying to five lenders at once, which shows up as multiple hard inquiries and can lower your credit score

- Assuming a debt consolidation loan will "fix" a spending habit — it only fixes the structure of debt, not the behaviour behind it

Do's & Don'ts

Do's:

- Do compare at least 3 lenders before applying

- Do check your CIBIL score before you start

- Do read the loan agreement fully, including fine print on charges

- Do set up auto-debit for the new EMI immediately

- Do keep proof of old debt closure safely for at least 2 years

Don'ts:

- Don't apply to multiple lenders simultaneously without spacing it out

- Don't ignore the tenure — a "smaller EMI" can be a trap

- Don't keep old credit cards active with high limits after consolidation

- Don't skip reading about prepayment charges

- Don't fall for lenders promising "guaranteed approval, no documents" — this is a red flag in India's lending space

Myths vs Facts

Myth | Fact |

| "Debt consolidation reduces the total amount I owe." | It doesn't reduce your principal debt — it restructures it into one loan, ideally at a lower rate. |

| "Only people with bad credit need debt consolidation." | Even good-credit borrowers use it to simplify multiple EMIs and cut interest costs. |

| "It will permanently damage my credit score." | A hard inquiry causes a small, temporary dip. Consistent repayment afterward typically improves your score over 6–12 months. |

| "All debt consolidation companies in India are the same." | Rates, fees, and tenure flexibility vary significantly between banks and NBFCs — comparison matters. |

| "Once I consolidate, I'm debt-free." | You still owe the full consolidated amount — you've just organised it better. |

Frequently Asked Questions

1. What is the best way to consolidate debt in India? The best method depends on your debt type — personal loans work well for credit card and unsecured loan debt, while loan against property suits larger amounts if you own property.

2. Can I consolidate credit card debt only? Yes. Many banks offer balance transfer facilities specifically for credit card debt, sometimes with an introductory low-interest period. See our dedicated credit card debt consolidation loan guide for card-specific offers.

3. Is debt consolidation the same as debt settlement? No. Debt consolidation means taking a new loan to pay off old debts in full. Debt settlement means negotiating with creditors to pay less than what's owed — this is uncommon and riskier in India's formal lending system.

4. Will debt consolidation hurt my credit score? There's usually a small, short-term dip from the credit inquiry. Over time, timely EMI payments on one consolidated loan tend to improve your score.

5. What credit score do I need for debt consolidation loans in India? Most banks prefer 650 and above; a score of 750+ gets you the best rates. NBFCs may accept scores as low as 600 at higher interest rates.

6. How much can I borrow for debt consolidation? This depends on income and lender, but ranges from ₹50,000 up to ₹40–55 lakh with top private banks and NBFCs.

7. Are there debt consolidation companies specifically for salaried employees? Most banks and NBFCs cater to salaried employees, often with faster approvals if your salary account is with the same bank.

8. Can self-employed individuals get debt consolidation loans? Yes, with ITR and business proof documentation. Rates may be slightly higher due to perceived income variability.

9. What happens if I miss an EMI on my consolidation loan? You'll incur late payment charges and it will negatively affect your credit score, similar to any other loan default.

10. Is it better to consolidate through a bank or an NBFC? Banks typically offer lower rates but stricter eligibility. NBFCs approve faster and are more flexible but usually charge higher interest.

11. Can I consolidate a mix of secured and unsecured loans? Generally, debt consolidation loans work best for unsecured debts (credit cards, personal loans). Secured loans like home loans usually aren't merged in.

12. Do I need collateral for debt consolidation loans? Most personal loan-based consolidation is unsecured, needing no collateral. Loan against property requires collateral but offers lower rates.

13. How long does debt consolidation take in India? From application to disbursal, it typically takes 1 to 7 working days depending on the lender and document readiness.

14. Can I get a debt consolidation loan with an existing personal loan? Yes, provided your total EMI obligation (including the new loan) stays within the lender's debt-to-income comfort zone, usually under 50-55%.

15. What is the maximum tenure for a debt consolidation loan? Most personal loan-based consolidation loans run 12 to 60 months; loan against property can extend up to 15–20 years.

16. Are there any tax benefits on debt consolidation loans? Generally no, since it's typically classified as a personal loan. Loan against property may offer limited tax benefits if funds are used for specified purposes — consult a tax advisor.

17. Can NRIs apply for debt consolidation loans in India? Some banks do offer this to NRIs with Indian income sources or co-applicants, but options are more limited than for resident Indians.

18. What if my consolidation loan application gets rejected? Check your credit report for errors, improve your debt-to-income ratio, or consider a co-applicant before reapplying — avoid applying to multiple lenders back-to-back.

19. Is it safe to consolidate debt through mobile lending apps? Only use RBI-registered NBFCs or apps listed on the RBI's official NBFC list. Verify registration before sharing documents or bank access.

20. Can debt consolidation actually save me money long-term? Yes, if your new interest rate is meaningfully lower than your blended old rate and you don't accumulate new debt on the accounts you just cleared.

Conclusion

Debt consolidation isn't a magic fix — it's a tool. Used well, it turns five scattered payments into one manageable EMI and can genuinely cut your interest cost, the way it did for Priya. Used carelessly, it just moves the same problem to a new lender with a longer tenure.

The best debt consolidation companies in India for 2026 are the ones that are transparent about total cost — not just the EMI, but the processing fee, the foreclosure terms, and the total interest over the full tenure.

Before you sign anything, do the math, compare at least three lenders, and be honest with yourself about whether the old credit cards are staying closed for good.